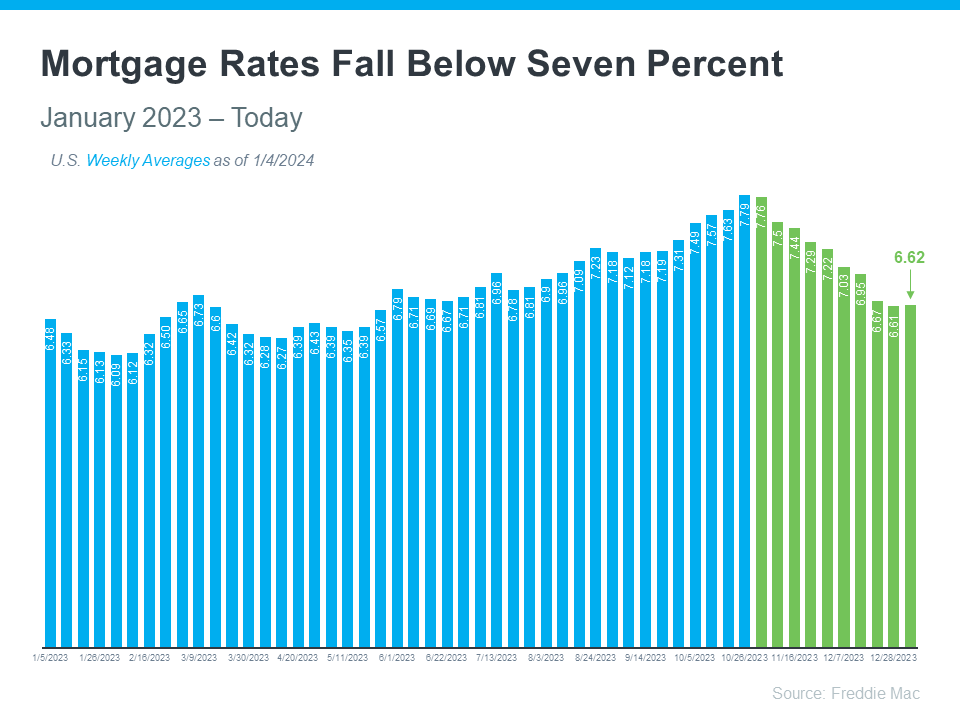

If you want to buy a home, it’s important to know how mortgage rates impact what you can afford and how much you’ll pay each month. Fortunately, rates for 30-year fixed mortgages have come down significantly since the end of October and are currently under 7%, according to Freddie Mac (see graph below):

This recent trend is great news for buyers. As a recent article from Bankratesays:

“The rate cool-off somewhat eases the housing affordability squeeze.”

And according to Edward Seiler, AVP of Housing Economics and Executive Director of the Research Institute for Housing America at the Mortgage Bankers Association (MBA):

“MBA expects that affordability conditions will continue to improve as mortgage rates decline . . .”

Here’s a bit more context on how this could help with your plans to buy a home.

How Mortgage Rates Affect Your Search for a Home

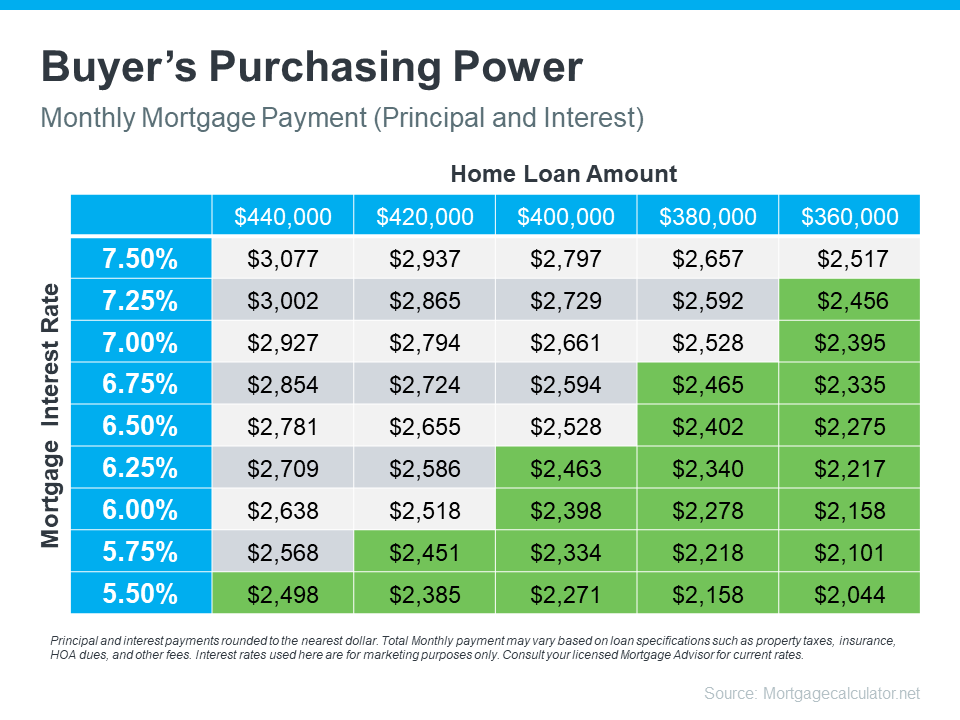

Understanding the connection between mortgage rates and your monthly home payment is crucial for your plans to become a homeowner. The chart below illustrates how your ability to afford a home changes when mortgage rates shift. Imagine your budget allows for a monthly payment between $2,400 and $2,500. The green part in the chart shows payments in that range or lower (see chart below):

As you can see, even small changes in rates can affect your budget and the loan amount you can afford.

Get Help from Reliable Experts To Understand Your Budget and Plan Ahead

When you’re looking to buy a home, it’s important to get guidance from a local real estate agent and a trusted lender. They can help you explore different mortgage options, understand what makes mortgage rates go up or down, and how those changes impact you.

By looking at the numbers and the latest data together, then adjusting your strategy based on today’s rates, you’ll be better prepared and ready to buy a home.

Bottom Line

If you’re looking to buy a home, you should know the recent downward trend in mortgage rates is good news for your move. Let’s connect and plan your next steps.

If you’re planning to buy a home, knowing what to budget for and how to save may sound intimidating – but it doesn’t have to be. One way to ease those concerns is to make sure you understand some of the costs you may encounter up front. And to do that, always turn to trusted real estate professionals. They can help you set a plan and take a strategic look at your budget and your process before you even get started.

Here are just a few things experts say you should be thinking about.

1. Down Payment

Saving for your down payment is likely top of mind as you set out to buy a home. But do you know how much you’ll need? While every buyer’s situation is different, there’s a common misconception that putting 20% of the purchase price down is required. An article from the Mortgage Reportsexplains why that’s not always the case:

“The idea that you have to put 20% down on a house is a myth. . . . The right amount depends on your current savings and your home buying goals.”

To understand your options, partner with trusted real estate professionals to go over the various loan types, down payment assistance programs, and what each one requires. The more you know ahead of time, the easier the process will be.

2. Closing Costs

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various parties involved in your transaction. Bankrateexplains:

“Closing costs are the fees you pay when finalizing a real estate transaction, whether you’re refinancing a mortgage or buying a new home. These costs can amount to 2 to 5 percent of the mortgage so it’s important to be financially prepared for this expense.”

The best way to understand what you’ll need at the closing table is to work with a trusted lender. They can provide you with answers to the questions you might have.

3. Earnest Money Deposit

If you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). An EMD is money you pay as a show of good faith when you make an offer on a house. According to Realtor.com, it’s usually between 1% and 2% of the total home price.

This deposit works like a credit. It’s not an added expense – it’s paying a portion of your costs upfront. You’re using some of the money you’ve already saved for your purchase to show the seller you’re committed and serious about buying their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, an EMD isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your local area. They’ll advise you on what moves you should make so you can make the best possible decisions throughout the buying process.

Bottom Line

When buying a home, being informed about what to save for is key. Let’s connect so you’ll have an expert on your side to answer any questions you have along the way.

If you’ve recently decided you’re ready to become a homeowner, chances are you’re trying to figure out what to do first. It can feel a bit overwhelming to know where to start, but the good news is you don’t have to navigate all of that alone.

When it comes to buying a home, there are a lot of moving pieces. And that’s especially true in today’s housing market. The number of homes for sale is still low, and home prices and mortgage rates are still high. That combination can be tricky if you don’t have reliable expertise and a trusted advisor on your side. That’s why the best place to start is connecting with a local real estate agent.

Agents Are the #1 Most Useful Source in the Buying Process

The latest annual report from the National Association of Realtors (NAR) finds recent homebuyers agree the #1 most useful source of information they had in the home buying process was a real estate agent. Let’s break down why.

How an Agent Helps When You Buy a Home

When you think about a real estate agent, you may think of someone taking you on home showings and putting together the paperwork, but a great agent does so much more than that. It’s not just being the facilitator for your purchase, it’s being your guide through every step.

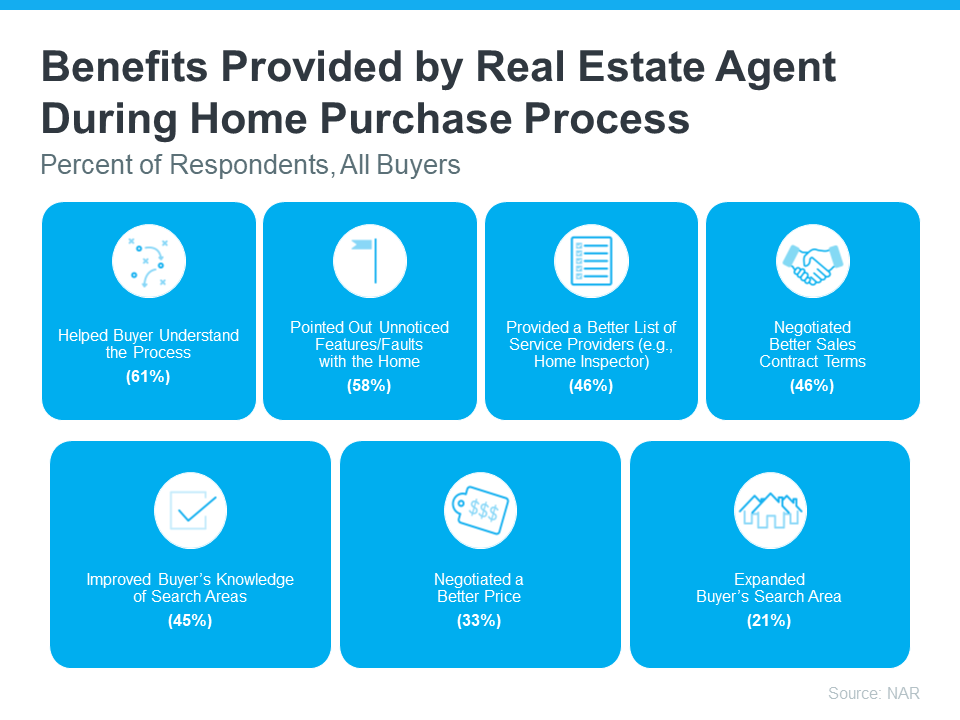

The visual below shows some examples from that same NAR release of the many ways an agent adds value. It includes the percentage of homebuyers in that report who highlighted each of these benefits:

Here’s a bit more context on how the survey results noted an agent continually helps buyers in these situations:

Helped Buyer’s Understand the Process: Do you know the difference between an inspection and an appraisal, what each report tells you, and why they’re both important? Or that there are things you shouldn’t do after applying for a mortgage, like buying appliances or furniture? An agent knows all of these best practices and will share them with you along the way, so you don’t miss any key steps by the time you get to the closing table.

Pointed Out Unnoticed Features or Faults with the Home: An agent also has a lot of experience evaluating homes. They’ve truly seen it all. They’ll be able to pinpoint some things you may not have noticed about the home that could help inform your decision or at least what repairs you ask for.

Provided a Better List of Service Providers: In a real estate transaction, there are a lot of people involved. An agent has experience working with various professionals in your area, like home inspectors, and can help connect you with the pros you need for a successful experience.

Negotiated Better Contract Terms and Price: Did something pop up in the home inspection or with the appraisal? An agent will help you re-negotiate as needed to get the best terms and price possible for you, so you feel confident with your big purchase.

Improved Buyer’s Knowledge of the Search Area: Moving to a new town and you’re not familiar with the area, or you’re staying nearby, but don’t know which neighborhoods are most affordable? Either way, an agent knows the local area like the back of their hand and can help you find the perfect location for your needs.

Expanded Buyer’s Search Area: And if you’re not finding anything you’re interested in within your initial search radius, an agent will know other neighborhoods nearby you should consider based on what you like, what amenities you want, and more.

Bottom Line

If you’re looking to buy a home, don’t forget about the many ways an agent is essential to that process. Any hurdle that pops up, a negotiation that needs to take place, and more, your agent will know how to handle it while they make sure to minimize your stress along the way. Let’s connect to tackle this together.

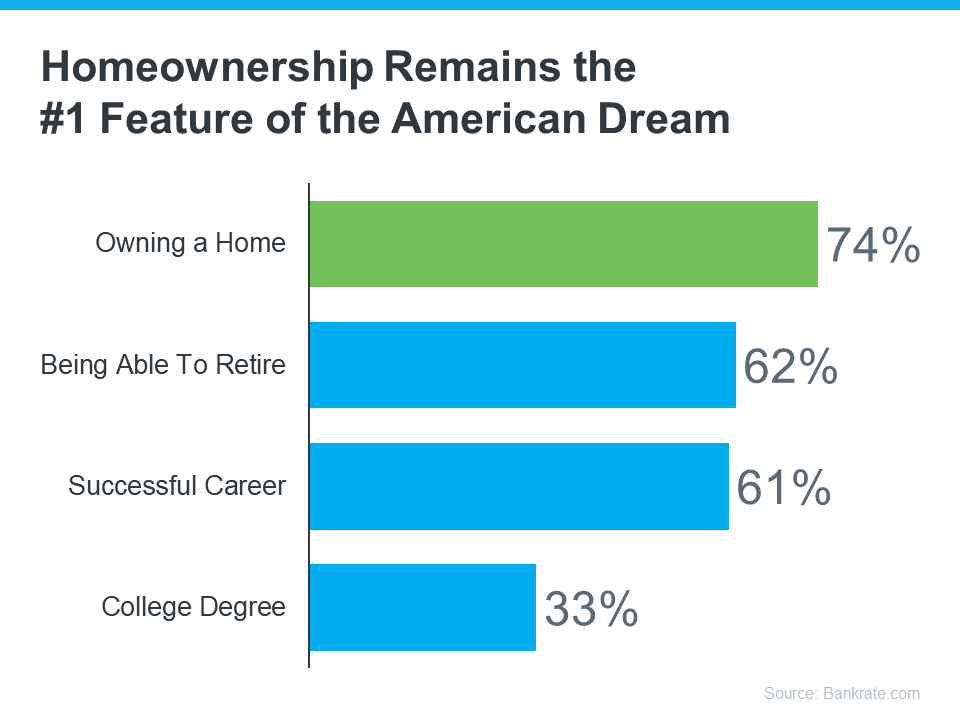

Everyone has their own idea of the American Dream, and it’s different for each person. But, in a recent survey by Bankrate, people were asked about the achievements they believe represent the American Dream the most. The answers show that owning a home still claims the #1 spot for many Americans today (see graph below):

In fact, according to the graph, owning a home is more important to people than retiring, having a successful career, or even getting a college degree. But is the dream of homeownership still alive for younger generations?

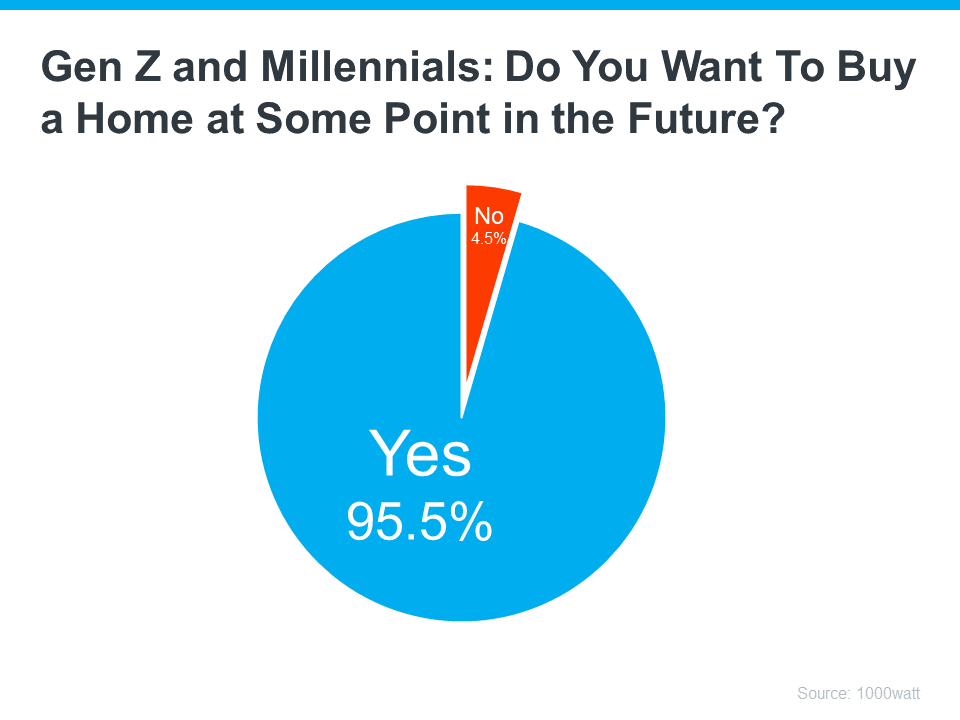

A recent survey by 1000watt dives into how the two generations many people believed would be the renter generations (Gen Z and millennials) feel about homeownership. Specifically, it asks if they want to buy a home in the future. The resounding answer is yes (see graph below):

While there are plenty of reasons why someone might prefer homeownership to renting, the same 1000watt survey shows, that for 63% of Gen Z and millennials, it’s that your place doesn’t feel like “home” unless you own it – maybe you feel the same way.

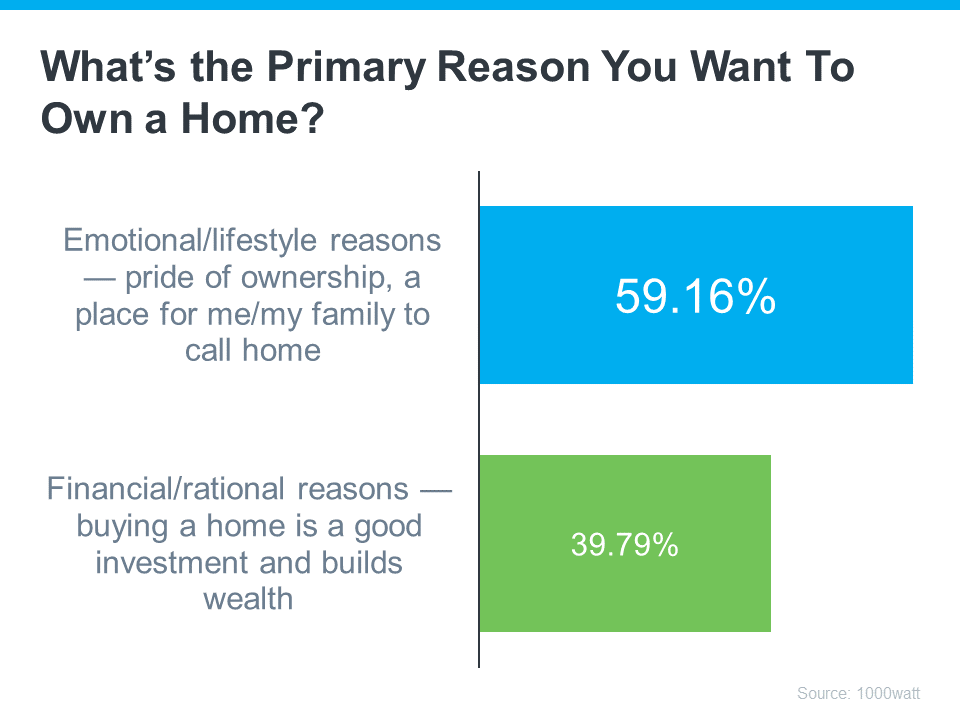

That emotional draw is further emphasized when you look at the reasons why Gen Z and millennials want to become homeowners. For all the financial benefits homeownership provides, in most cases it’s about the lifestyle or emotional benefits (see graph below):

What Does This Mean for You?

If you’re a part of Gen Z or are a millennial and you’re ready, willing, and able to buy a home, you’ll want a great real estate agent by your side. Their experience and expertise in the local housing market will help you overcome today’s high mortgage rates, low inventory, and rising home prices to find your first home and turn your dream into a reality.

Working with a local real estate agent to find your dream home is the key to unlocking the American Dream.

Bottom Line

Buying a home is a big, important decision that represents the heart of the American Dream. If you want to accomplish your goal, let’s connect to start the process today.

Mortgage rates have been back on the rise recently and that’s getting a lot of attention from the press. If you’ve been following the headlines, you may have even seen rates recently reached their highest level in over two decades (see graph below):

That can feel like a little bit of a gut punch if you’re thinking about making a move. If you’re wondering whether or not you should delay your plans, here’s what you really need to know.

How Higher Mortgage Rates Impact You

There’s no denying mortgage rates are higher right now than they were in recent years. And, when rates are up, that affects overall home affordability. It works like this. The higher the rate, the more expensive it is to borrow money when you buy a home. That’s because, as rates trend up, your monthly mortgage payment for your future home loan also increases.

Urban Instituteexplains how this is impacting buyers and sellers right now:

“When mortgage rates go up, monthly housing payments on new purchases also increase. For potential buyers, increased monthly payments can reduce the share of available affordable homes . . . Additionally, higher interest rates mean fewer homes on the market, as existing homeowners have an incentive to hold on to their home to keep their low interest rate.”

Basically, some people are deciding to put their plans on hold because of where mortgage rates are right now.But what you want to know is: is that a good strategy?

Where Will Mortgage Rates Go from Here?

If you’re eager for mortgage rates to drop, you’re not alone. A lot of people are waiting for that to happen. But here’s the thing. No one knows when it will. Even the experts can’t say with certainty what’s going to happen next.

Forecasts project rates will fall in the months ahead, but what the latest data says is that rates have been climbing lately. This disconnect shows just how tricky mortgage rates are to project.

The best advice for your move is this: don’t try to control what you can’t control. This includes trying to time the market or guess what the future holds for mortgage rates. As CBS Newsstates:

“If you’re in the market for a new home, experts typically recommend focusing your search on the right home purchase — not the interest rate environment.”

Instead, work on building a team of skilled professionals, including a trusted lender and real estate agent, who can explain what’s happening in the market and what it means for you. If you need to move because you’re changing jobs, want to be closer to family, or are in the middle of another big life change, the right team can help you achieve your goal, even now.

Bottom Line

The best advice for your move is: don’t try to control what you can’t control – especially mortgage rates. Even the experts can’t say for certain where they’ll go from here. Instead, focus on building a team of trusted professionals who can keep you informed. When you’re ready to get the process started, let’s connect.

Shawna O’Brien Keller Williams Portfolio 317-506-0039 ShawnaOBrienRealtor@gmail.com

The housing market is affected by many factors, from the economy to interest rates to local supply and demand. But did you know that the time of year can influence the final sale price of a home?

Believe it or not, home prices vary by the season. So when is the best time of year to buy a house? Here’s how the housing market changes during the course of the year.

Spring Home-Buying Season

The spring and summer months tend to be a seller’s market. Spring, especially, is a hot selling season due to the pent-up demand from the winter months. Additionally, the warmer weather often encourages home buyers to start their house hunt, and the budding flowers and trees add curb appeal to homes entering the market.

As a homebuyer, you’ll need to have a strong offer at the ready; that means more than just having enough money to cover the purchase price and closing costs. Many sellers won’t even consider an offer unless you have a pre-approval letter from a trustworthy lender. Even then, you may find yourself in a bidding war due to higher demand.

On the other hand, spring brings an increase in available homes, which can give buyers more choices. According to the National Association of Realtors, the number of homes jumped from 850,000 to 930,000 between February and March of 2021, reaching 1.15 million by May.

Summer Home-Buying Season

In many ways, the summer months are a continuation of the spring. Buyers can expect a higher number of homes for sale, though they’ll also face strong competition with others looking to buy a home between June and August.

But there’s an upside to buying a home during the summer. Many of the homes on the market are left over from spring, and sellers may be eager to close on their homes before September rolls around and the school year begins. Therefore, if you can wait until August, you may be able to find a motivated seller who is willing to offer you a reduced sales price.

These summer trends are also climate-dependent. The sweltering heat of places like Florida or Texas can discourage buyers from shopping in earnest, so you may discover that your local market is more or less affected by summer, depending on your distance from the equator.

Fall Home-Buying Season

Fall is very much a buyer’s market and can potentially be your best time to shop. Once summer ends, sellers can be motivated to sell their homes, especially if they want to use them as a tax write-offs before the end of the year.

Doesn’t that mean you’ll face less selection? Yes, it’s possible, depending on your region. However, the National Association of Realtors (NAR) reports that in 2021, there were more homes available between September and November (1.2 million, on average) than between March and May (1.1 million). Consequently, fall might actually be your prime buying season.

When is the best time to buy a home during the fall? Data from the NAR shows that in 2021, housing prices dropped from $361,500 in August to $355,100 in September. This makes September your optimal choice, though prices only increase by a few hundred dollars during October and November.

Winter Home-Buying Season

Winter can be an unusual time to buy a home, especially since the calendar year changes in January.

On the one hand, many sellers suspend their listings between Thanksgiving and the New Year, believing that buyers are too scarce. But the sellers who continue to list may be particularly motivated to sell their homes prior to January, which may give you an edge.

However, there are some challenges to buying a house in winter. If you live in a cold climate, snowstorms can interfere with your ability to visit various properties and can also make it difficult for home inspectors to examine roofs and other structures.

Furthermore, once January hits, sellers may no longer be quite as motivated to sell their homes and may prefer to wait a few months until the seller’s market in the spring.

Buying a home early in the winter can help you save, but you may face challenges the longer you wait.

Tips for When to Buy a House

Real estate markets fluctuate by season, but there are other personal and economic factors to consider when buying a home. Here are some tips that can guide you through the process.

Are You Ready to Buy a House?

When is the best time to buy a house? When you’re ready. To that end, make sure you consider such factors as:

Having enough savings for a down payment and closing costs

Improving your credit score to secure favorable interest rates

Plan to keep the same job through the buying process

Paying off any outstanding debt

If your credit score is low or you carry a lot of household debt, it may be wise to work on these issues before starting your home search. A low credit score or high debt-to-income ratio can jeopardize your chances at favorable mortgage terms and leave you stuck with higher mortgage rates.

What Are the Current Market Conditions?

Before you start shopping, take a look at the following key metrics:

Average home price in your area

Current mortgage rates

The supply of homes in your area

For example, when the U.S. Federal Reserve raised interest rates in 2022, mortgage rates went up nationwide. With the economy beginning to stabilize, home buyers are now able to re-enter the market and obtain homes with affordable rates and terms.

What Is the Local Inventory?

Research the number and type of available homes in your area or the area you want to move to. A large inventory of homes will give you more options and will also prevent you from having to compete with other buyers.

As you’ve seen, housing supply can be affected by the calendar year. Don’t get discouraged if you can’t find your dream home in February. By May or June, you may find a home that fits your needs. If you hold out until fall, you could even find the deal of a lifetime.

How to Get a Mortgage Pre-Approval

Getting pre-approved for a mortgage will give you a clear picture of your purchasing budget and give your offer more weight in sellers’ eyes. During the pre-approval process, you’ll submit some basic financial information and submit to a credit check.

Once approved, you’ll receive a pre-approval letter that outlines the basics of your prospective loan. Just be aware that no loan is official until you receive final approval from your lender.

The “Perfect” Time to Buy a House

Ultimately, there’s no single best time to buy a house. But if you understand your needs and the state of the market, you can time your purchase to your advantage. For more assistance with the pre-approval process, contact me today.

You might remember the housing crash in 2008, even if you didn’t own a home at the time. If you’re worried there’s going to be a repeat of what happened back then, there’s good news – the housing market now is different from 2008.

One important reason is there aren’t enough homes for sale. That means there’s an undersupply, not an oversupply like the last time. For the market to crash, there would have to be too many houses for sale, but the data doesn’t show that happening.

Housing supply comes from three main sources:

Homeowners deciding to sell their houses

Newly built homes

Distressed properties (foreclosures or short sales)

Here’s a closer look at today’s housing inventory to understand why this isn’t like 2008.

Homeowners Deciding To Sell Their Houses

Although housing supply did grow compared to last year, it’s still low. The current months’ supply is below the norm. The graph below shows this more clearly. If you look at the latest data (shown in green), compared to 2008 (shown in red), there’s only about a third of that available inventory today.

So, what does this mean? There just aren’t enough homes available to make home values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that’s not happening right now.

Newly Built Homes

People are also talking a lot about what’s going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. The graph below shows the number of new houses built over the last 52 years:

The 14 years of underbuilding (shown in red) is a big part of the reason why inventory is so low today. Basically, builders haven’t been building enough homes for years now and that’s created a significant deficit in supply.

While the final blue bar on the graph shows that’s ramping up and is on pace to hit the long-term average again, it won’t suddenly create an oversupply. That’s because there’s too much of a gap to make up. Plus, builders are being intentional about not overbuilding homes like they did during the bubble.

Distressed Properties (Foreclosures and Short Sales)

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back during the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from the Federal Reserve to show how things have changed since the housing crash:

This graph illustrates, as lending standards got tighter and buyers were more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures and the forbearance program helped prevent a repeat of the wave of foreclosures we saw back around 2008.

The forbearance program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. And data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

What This Means for You

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. According to Bankrate, that isn’t going to change anytime soon, especially considering buyer demand is still strong:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equationsimply won’t allow a price crash in the near future.”

Bottom Line

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing inventory tells us there’s no crash on the horizon.

Shawna O’Brien, Executive Club F.C. Tucker Geist Fishers shawna.obrien@talktotucker.com 317-506-0039

If you’re looking to buy a home this fall, there are a few things you need to know. Affordability is tight with today’s mortgage rates and rising home prices. At the same time, there’s a limited number of homes on the market right now and that’s creating some competition among buyers. But, if you’re strategic, there are ways to navigate these waters. The first thing you’ll want to do is get pre-approved for a mortgage. That way you’ll know your numbers and can set yourself up for success from the start of your home search.

What Pre-Approval Does for You

To understand why it’s such an important step, you need to know what pre-approval is. As part of the homebuying process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you know how much money you can borrow. Freddie Macexplains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow. Why does this help you, especially today? With higher mortgage rates and home prices impacting affordability for many buyers right now, a solid understanding of your numbers is even more important so you can truly wrap your head around your options.

Pre-Approval Helps Show Sellers You’re a Serious Buyer

Let’s face it, there are more buyers looking to buy than there are homes available for sale and that imbalance is creating some competition among homebuyers. That means you could see yourself in a multiple-offer scenario when you make an offer on a home. But getting pre-approved for a mortgage can help you stand out from other hopeful buyers.

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Pre-approval shows the seller you’re a serious buyer that’s already undergone a credit and financial check, making it more likely that the sale will move forward without unexpected delays or financial issues.

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. The more prepared you are, the better chance you have of getting the home you want. Connect with a trusted lender so you have the tools you need to purchase a home in today’s market.

Shawna O’Brien, Executive Club F.C. Tucker Geist Fishers shawna.obrien@talktotucker.com 317-506-0039

The way Americans work has changed in recent years, and remote work is at the forefront of this shift. Experts say it’ll continue to be popular for years to come and project that 36.2 million Americans will be working remotely by 2025. To give you some perspective, that’s a 417% increase compared to the pre-pandemic years when there were just 7 million remote workers.

If you’re in the market to buy a home and you work remotely either full or part-time, this trend is a game-changer. It can help you overcome some of today’s affordability and housing inventory challenges.

How Remote Work Helps with Affordability

Remote or hybrid work allows you to change how you approach your home search. Since you’re no longer commuting every day, you may not feel it’s as essential to live near your office. If you’re willing to move a bit further out in the suburbs instead of the city, you could open up your pool of affordable options. In a recent study, Fannie Maeexplains:

“Home affordability may also be a reason why we saw an increase in remote workers’ willingness to relocate or live farther away from their workplace . . .”

If you’re thinking about moving, having this kind of location flexibility can boost your chances of finding a home that fits your budget. Work with your agent to cast a wider net that includes additional areas with a lower cost of living.

More Work Flexibility Means More Home Options

And as you broaden your search to include more affordable options, you may also find you have the chance to get more features for your money too. Given the low supply of homes for sale, finding a home that fits all your wants and needs can be challenging.

By opening up your search, you’ll give yourself a bigger pool of options to choose from, and that makes it easier to find a home that truly fits your lifestyle. This could include homes with more square footage, diverse home styles, and a wider range of neighborhood amenities that were previously out of reach.

Historically, living close to work was a sought-after perk, often coming with a hefty price tag. But now, the dynamics have changed. If you work from home, you have the freedom to choose where you want to live without the burden of long daily commutes. This shift allows you to focus more on finding a home that is affordable and delivers on your dream home features.

Bottom Line

Remote work goes beyond job flexibility. It’s a chance to broaden your horizons in your home search. Without being bound to a fixed location, you have the freedom to explore all of your options. Let’s connect to find out how this freedom can lead you to your ideal home.

Shawna O’Brien, Executive Club F.C. Tucker Geist Fishers shawna.obrien@talktotucker.com 317-506-0039