Applying for a mortgage is a big step towards homeownership, but it doesn’t need to be one you fear. Here are some tips to help you prepare.

Know your credit score and work to build strong credit. When you’re ready, lean on your agent to connect you with a lender so you can get pre-approved and begin your home search.

Any major life change can be scary, and buying a home is no different. Let’s connect so you have an advisor by your side to take the fear out of the equation.

While today’s supply of homes for sale is still low, the number of newly built homes is increasing. If you’re ready to sell but have held off because you weren’t sure you’d be able to find a home to move into, newly built homes and those under construction can provide the options you’ve been waiting for.

The latest Census data shows the inventory of new homes is increasing this year (see graph below):With more new homes coming to the market, this means you’ll have more options to choose from if you’re ready to buy. Of course, if you do consider a newly built home, you’ll want to keep timing in mind. The supply shown in the graph above includes homes at various stages of the construction process – some are near completion while others may be months away.

“28% of new home inventory consists of homes that have not started construction, compared to 21% a year ago.”

Buying a home near completion is great if you’re ready to move. Alternatively, a home that has yet to break ground might benefit you if you’re ready to sell and you aren’t on a strict timeline. You’ll have an even greater opportunity to design your future home to suit your needs. No matter what, your trusted real estate advisor can help you find a home that works for you.

Bottom Line

If you want to take advantage of today’s sellers’ market, but you’re not sure if you’ll be able to find a home to move into, consider a newly built home. Let’s connect today so you have a trusted real estate advisor to guide you through the sale of your house and discuss your homebuying options.

Buyers in today’s market often have questions about the importance of getting a home appraisal and an inspection. That’s because high buyer demand and low housing supply are driving intense competition and leading some buyers to consider waiving those contingencies to stand out in the crowded market.

But is that the best move? Buying a home is one of the most important transactions in your lifetime, and it’s critical to keep your best interests in mind. Here’s a breakdown of what to expect from the appraisal and the inspection, and why each one can potentially save you a lot of time, money, and headaches down the road.

Home Appraisal

The home appraisal is a critical step for securing a mortgage on your home. As Home Light explains:

“. . . lenders typically require an appraisal to ensure that your loan-to-value ratio falls within their underwriting guidelines. Mortgages are secured loans where the lender uses your home as collateral in case you default on the agreed-upon payments.”

Put simply: when you apply for a mortgage, an unbiased appraisal – typically required by your lender – is the best way to verify the value of the home. That appraisal ensures the lender doesn’t loan you more than what the home is worth.

When buyers are competing like they are today, bidding wars and market conditions can push prices up. A buyer’s contract price may end up higher than the value of the home – this is known as an appraisal gap. In today’s market, it’s common for the seller to ask the buyer to make up the difference when an appraisal gap occurs. That means, as a buyer, you may need to be prepared to bring extra money to the table if you really want the home.

Home Inspection

Like the appraisal, the inspection is important because it gives an impartial evaluation of the home. While the appraisal determines the current value of the home, the inspection determines the current condition of the home. As the American Society of Home Inspectors puts it:

“Home inspections are the opportunity to discover major defects that were not apparent at a buyer’s showing. . . . Your home inspection is to help you make an informed decision about the house, including its condition.”

If there are any concerns during the inspection – an aging roof, a malfunctioning HVAC system, or any other questionable items – you have the option to discuss and negotiate any potential issues with the seller. Your real estate advisor can help you navigate this process and negotiate what, if any, repairs need to be made before the sale is finalized.

Keep in mind – home inspections are critical because they can shed light on challenges you may face as the new homeowner. Without an inspection, serious, sometimes costly issues could come as a surprise later on.

Bottom Line

Both the appraisal and the inspection are important steps in the homebuying process. They protect your best interests as a buyer by providing unbiased information about the home’s value and condition. Let’s connect so you have an expert guiding you throughout the entire process.

The last 18 months changed what many buyers are looking for in a home. Recently, the American Institute of Architects released their AIA Home Design Trends Survey results for Q3 2021. The survey reveals the following:

70% of respondents want more outdoor living space

69% of respondents want a home office (48% wanted multiple offices)

46% of respondents want a multi-function room/flexible space

42% of respondents want an au pair/in-law suite

39% of respondents want an exercise room/yoga space

If you’re a homeowner who wants to add any of the above, you have two options: renovate your current house or buy a home that already has the spaces you desire. The decision you make could be determined by factors like:

A possible desire to relocate

The difference in the cost of a renovation versus a purchase

Finding an existing home or designing a new home that has exactly what you want (versus trying to restructure the layout of your current house)

In either case, you’ll need access to capital: the funds for the renovation or the down payment your next home would require. The great news is that the money you need probably already exists in your current home in the form of equity.

Home Equity Is Skyrocketing

The record-setting increases in home prices over the last two years dramatically improved homeowners’ equity. The graph below uses data from CoreLogic to show the average home equity gain in the first quarter of the last nine years:Odeta Kushi, Deputy Chief Economist at First American,quantifies the amount of equity homeowners gained recently:

“Remember U.S. households own nearly $35 trillion in owner-occupied real estate, just over $11 trillion in debt, and the remaining ~$24 trillion in equity. In inflation adjusted terms, homeowners in Q2 had an average of $280,000 in equity- a historic high.”

As a homeowner, the money you need to purchase the perfect home or renovate your current house may be right at your fingertips. However, waiting to make your decision may increase the cost of tapping that equity.

If you decide to renovate, you’ll need to refinance (or take out an equity loan) to access the equity. If you decide to move instead and use your equity as a down payment, you’ll still need to mortgage the remaining difference between the down payment and the cost of your next home.

Mortgage rates are forecast to increase over the next year. Waiting to leverage your equity will probably mean you’ll pay more to do so. According to the latest data from the Federal Housing Finance Agency (FHFA), almost 57% of current mortgage holders have a mortgage rate of 4% or below. If you’re one of those homeowners, you can keep your mortgage rate under 4% by doing it now. If you’re one of the 43% of homeowners with a mortgage rate over 4%, you may be able to do a cash-out refinance or buy a more expensive home without significantly increasing your monthly payment.

First Step: Determine the Amount of Equity in Your Home

If you’re ready to either redesign your current house or find an existing or newly constructed home that has everything you want, the first thing you need to do is determine how much equity you have in your current home. To do that, you’ll need two things:

The current mortgage balance on your home

The current value of your home

You can probably find the mortgage balance on your monthly mortgage statement. To find the current market value of your house, you can pay several hundreds of dollars for an appraisal, or you can contact a local real estate professional who will be able to present to you, at no charge, a professional equity assessment report.

Bottom Line

If the past 18 months have refocused your thoughts on what you want from your house, now may be the time to either renovate or make a move to the perfect home.

The financial benefits of buying a home versus renting one are always up for debate. However, one element of the equation is often ignored – the ability to build wealth as a homeowner.

According to the latest research from the National Association of Realtors (NAR):

“Homeownership is a key pathway to building wealth and narrowing the racial income and wealth inequality gap. Housing wealth (equity) accumulation takes time and is built up by price appreciation and paying off the mortgage.”

An increase in equity builds the wealth of the individual that owns it. This wealth can be passed down to future generations. The Federal Reserve in an addendum to their Survey of Consumer Finances explains:

“There are numerous ways families can transmit wealth and resources across generations. Families can directly transfer their wealth to the next generation in the form of a bequest. They can also provide the next generation with inter vivos transfers (gifts), for example, providing down payment support to enable a home purchase or a substantial wedding gift.”

The Federal Reserve also explains another way wealth (including the additional net worth generated by an increase in home equity) can benefit future generations:

“In addition to direct transfers or gifts, families can make investments in their children that indirectly increase their wealth. For example, families can invest in their children’s educational success by paying for college or private schools, which can in turn increase their children’s ability to accumulate wealth.”

Here’s a look at how equity can build your wealth over time when you own a home.

Equity over the Last 30 Years

The NAR research reveals that the average gain for homeowners over the last five years was $139,134 and over the last 10 years was $218,505. Looking even further back in time, the article says:

“Homeowners who purchased a typical single-family existing-home 30 years ago at the median sales price of $103,333 with a 10% down payment loan and who sold the property at the median sales price of $357,700 in 2021 Q2 accumulated housing wealth of $349,258.”

Homeownership builds household wealth which also enables households to more easily move to the home of their dreams. As Mark Fleming, the Chief Economist at First American,explains:

“As homeowners gain equity in their homes, they are more likely to consider using that equity to purchase a larger or more attractive home – the wealth effect of rising equity.”

If you missed out on the equity gains over the last 30 years, don’t fret. Experts are still calling for substantial growth in equity over the next five years.

Looking Forward at the Equity To Come

The most recent Home Price Expectation Survey, a survey of over one hundred economists, real estate experts, and investment and market strategists, expects home values (and therefore equity) to increase as follows:

2021: 11.74%

2022: 5.82%

2023: 3.94%

2024: 3.56%

2025: 3.55%

The survey estimates a 31.8% cumulative appreciation over the next five years. Using their annual projections, the graph below shows the equity build-up a purchaser could earn, using a $350,000 home as an example:That’s a potential increase in household wealth of $111,285 over five years.

Bottom Line

Owning a home is one of the best ways to grow your wealth over time. House wealth can impact generations. In many cases, the largest single investment a household has is their home. As that investment appreciates in value, the financial options also increase.

10/7/2021 Sold a Single Family Home in 2121 in Indianapolis, IN.

Local knowledge ***** Process expertise ***** Responsiveness ***** Negotiation skills *****

Shawna was amazing from start to finish. She walked us thru every step. Her professionalism, work ethic and communication was the best in her field. You won’t find better!

Many memories were made in this home – 49 years worth for the homeowner! I also have a few memories in this home from my grade school years, hanging out with the seller’s daughter.

I was more then humbled and flattered when my long time friend asked me to help her mom sell her family home. Why choose me, out of all the realtors she knows in her community. It’s because she knew I would treat her mother like MY mother!

I treat everyone I help buy or sell a home the same as I would treat my Mother but it’s definitely special when I’m partnered with someone who really knows me and KNOWS I care and am invested in their best interest financially and emotionally.

Who has already purchased a pumpkin spiced latte? 😉 (Believe it or not, not me).

Whether you like all things pumpkin or not, I hope you are enjoying the season! My September born children both tell me that this is their favorite time of year, and they promise it’s the change of season, not because they get presents. 🙂

Do you know someone still renting? Rent continues to go up each year but when one purchases a home and locks in a rate for 30 years, the payment stays the same. The U.S. Median rental price has climbed nearly 10% year over year to $1,607. That is 15.5% higher than the monthly payments for a starter home, the lower-priced tier of homes for sale in a market. Yes there has been a recent jump in home prices but the low mortgage rates help offset that jump.

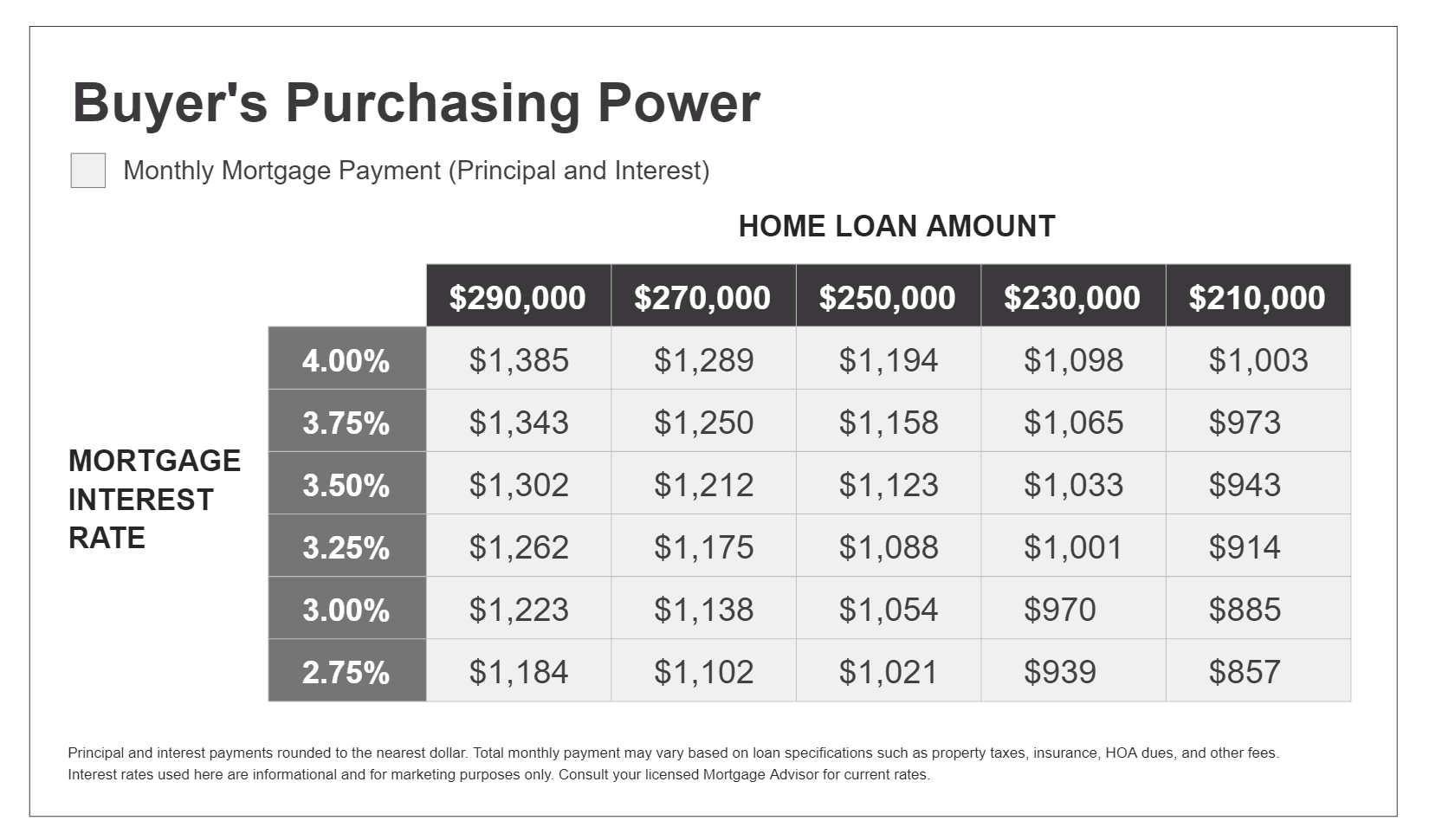

Here’s another visual to share with someone who is currently paying rent and wondering “How much do I need to budget each month to afford this house?”

The charts show the principle and interest payment dependent on the interest rate and loan amount.

Of course if you’re considering selling, we see the second highest activity behind the busy spring months. Pat and I coincidentally have purchased all three of the homes we’ve lived in together in the last 20 years in September, December, and November respectively.

I’m always here to help and answer any questions you have about the market. Give me a call, send an email or text or better yet, let me buy you a coffee (or pumpkin spice latte) and let’s catch up!

![The Mortgage Process Doesn’t Have To Be Scary [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/10/27142810/20211029-MEM-1046x1978.png)

.png) Of course if you’re considering selling, we see the second highest activity behind the busy spring months. Pat and I coincidentally have purchased all three of the homes we’ve lived in together in the last 20 years in September, December, and November respectively.

Of course if you’re considering selling, we see the second highest activity behind the busy spring months. Pat and I coincidentally have purchased all three of the homes we’ve lived in together in the last 20 years in September, December, and November respectively.