In the last few weeks, the average 30-year fixed mortgage rate from Freddie Mac inched up to 5%. While that news may have you questioning the timing of your home search, the truth is, timing has never been more important. Even though you may be tempted to put your plans on hold in hopes that rates will fall, waiting will only cost you more. Mortgage rates are forecast to continue rising in the year ahead.

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

How Rising Mortgage Rates Impact You

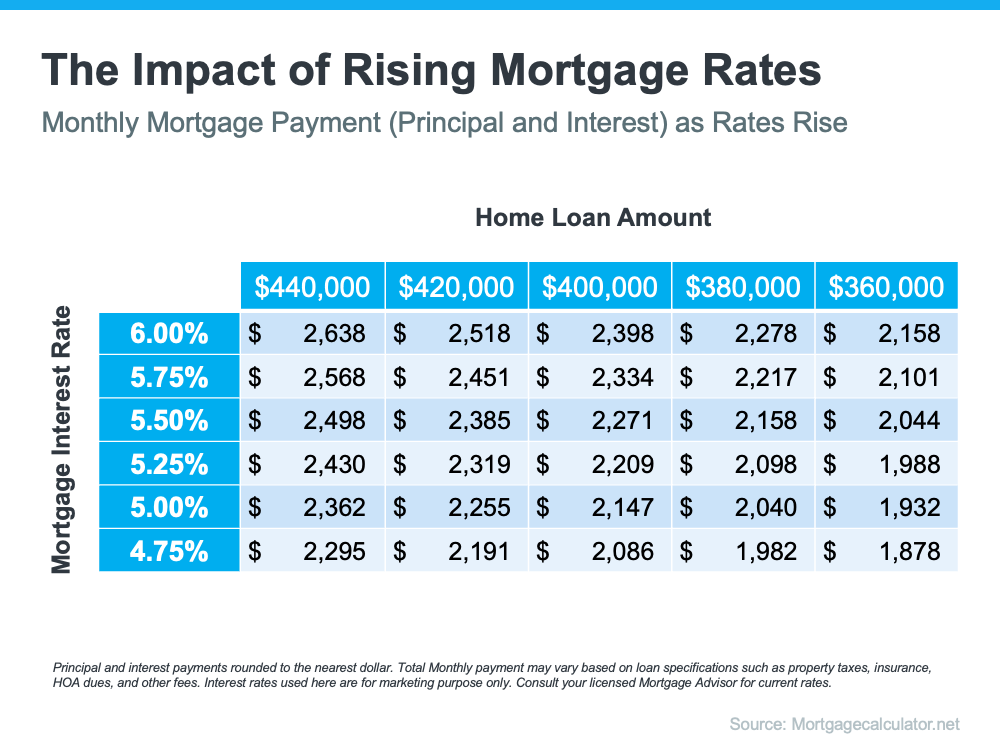

Mortgage rates play a significant role in your home search. As rates go up, they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. Here’s an example of how even a quarter-point increase can have a big impact on your monthly payment (see chart below):

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of delaying your plans, today’s rates should motivate you to purchase now before rates increase more. Use that motivation to energize your search and plan your next steps accordingly.

The best way to prepare is to work with a trusted real estate advisor now. An agent can connect you with a trusted lender, help you adjust your search based on your budget, and make sure you’re ready to act quickly when it’s time to make an offer.

Bottom Line

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Let’s connect today so you can better understand your budget and be prepared to buy your home even before rates climb higher.

There’s never been a truer statement regarding forecasting mortgage rates than the one offered last year by Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is: Don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

Coming into this year, most experts projected mortgage rates would gradually increase and end 2022 in the high three-percent range. It’s only April, and rates have already blown past those numbers. Freddie Macannounced last week that the 30-year fixed-rate mortgage is already at 4.72%.

“Continuing on the recent trajectory, would have mortgage rates hitting 5% within a matter of weeks. . . .”

Just five days later, on April 5, the Mortgage News Dailyquoted a rate of 5.02%.

No one knows how swiftly mortgage rates will rise moving forward. However, at least to this point, they haven’t significantly impacted purchaser demand. Ali Wolf, Chief Economist at Zonda, explains:

“Mortgage rates jumped much quicker and much higher than even the most aggressive forecasts called for at the end of last year, and yet housing demand appears to be holding steady.”

Through February, home prices, the number of showings, and the number of homes receiving multiple offers all saw a substantial increase. However, much of the spike in mortgage rates occurred in March. We will not know the true impact of the increase in mortgage rates until the March housing numbers become available in early May.

Rick Sharga, EVP of Market Intelligence at ATTOM Data, recently put rising rates into context:

“Historically low mortgage rates and higher wages helped offset rising home prices over the past few years, but as home prices continue to soar and interest rates approach five percent on a 30-year fixed rate loan, more consumers are going to struggle to find a property they can comfortably afford.”

While no one knows exactly where rates are headed, experts do think they’ll continue to rise in the months ahead. In the meantime, if you’re looking to buy a home, know that rising rates do have an impact. As rates rise, it’ll cost you more when you purchase a house. If you’re ready to buy, it may make sense to do so sooner rather than later.

Bottom Line

Mark Fleming got it right. Forecasting mortgage rates is an impossible task. However, it’s probably safe to assume the days of attaining a 3% mortgage rate are over. The question is whether that will soon be true for 4% rates as well.

As the spring housing market kicks off, you likely want to know what you can expect this season when it comes to buying or selling a house. While there are multiple factors causing some uncertainty, including the conflict overseas, rising inflation, and the first rate increase from the Federal Reserve in over three years — the housing market seems to be relatively immune.

Here’s a look at what experts say you can expect this spring.

1. Mortgage Rates Will Climb

Freddie Macreports the 30-year fixed mortgage rate has increased by more than a full point in the past six months. And despite some mild fluctuation in recent weeks, experts believe rates will continue to edge up over the next 90 days. As Freddie Macsays:

“The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year.”

If you’re a first-time buyer or a seller thinking of moving to a home that better fits your needs, realize that waiting will likely mean you’ll pay a higher mortgage rate on your purchase. And that higher rate drives up your monthly payment and can really add up over the life of your loan.

2. Housing Inventory Will Increase

There may be some relief coming for buyers searching for a home to purchase. Realtor.com recently reported that the number of newly listed homes has grown for each of the last two months. Also, the National Association of Realtors (NAR) just announced the months’ supply of inventory increased for the first time in eight months. The inventory of existing homes usually grows every spring, and it seems, based on recent activity, the next 90 days could bring more listings to the market.

If you’re a buyer who has been frustrated with the limited supply of homes available for sale, it looks like you could find some relief this spring. However, be prepared to act quickly if you find the right home.

If you’re a seller, listing now instead of waiting for this additional competition to hit the market makes sense. Your leverage in any negotiation during the sale will be impacted as additional homes come to market.

3. Home Prices Will Rise

Prices are always determined by supply and demand. Though the number of homes entering the market is increasing, buyer demand remains very strong. As realtor.com explains in their most recent Housing Report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

What does that mean for you? With the demand for housing still outpacing supply, home prices will continue to appreciate. Many experts believe the level of appreciation will decelerate from the high double-digit levels we’ve seen over the last two years. That means prices will continue to climb, just at a more moderate pace. Most experts are predicting home prices will not depreciate.

Won’t Increasing Mortgage Rates Cause Home Prices To Fall?

While some people may believe a 1% increase in mortgage rates will impact demand so dramatically that home prices will have to fall, experts say otherwise. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“What I will caution against is making the inference that interest rates have a direct impact on house prices. That is not true.”

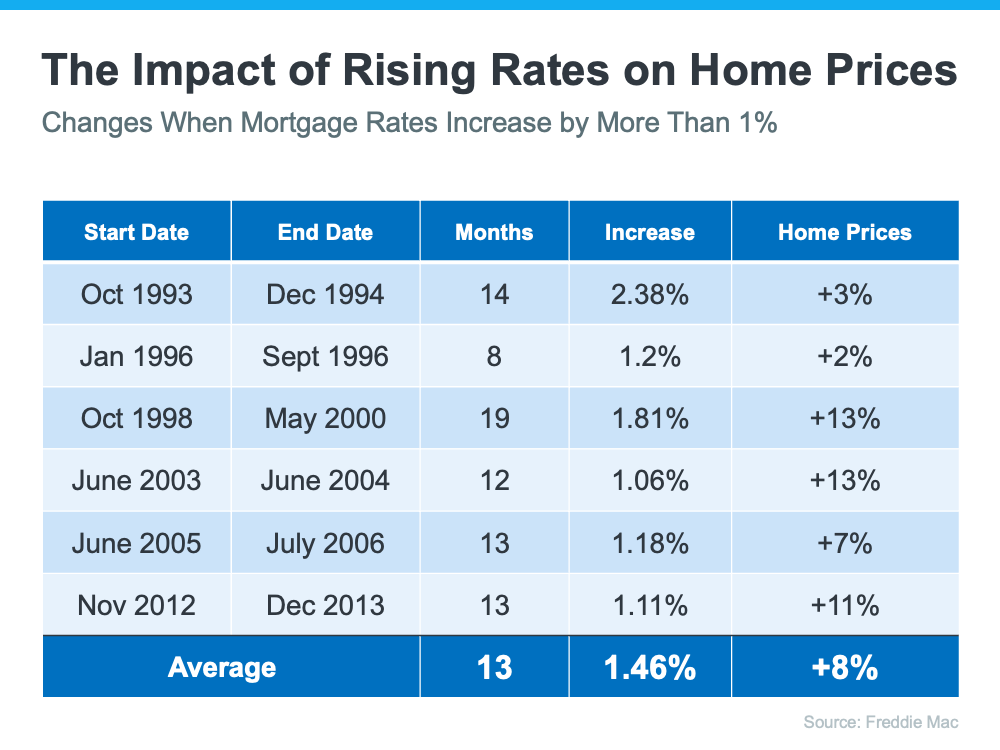

Freddie Mac studied the impact that mortgage rates increasing by at least 1% has had on home prices in the past. Here are the results of that study:

As the chart shows, mortgage rates jumped by at least 1% six times in the last thirty years. In each case, home values increased.

So again, if you’re a first-time buyer or a repeat buyer, waiting to buy likely means you’ll pay more for a home later in the year (as compared to its current value).

Bottom Line

There are three things that seem certain going into the spring housing market:

Mortgage rates will continue to rise

The selection of homes available for sale will modestly improve

Home prices will continue to appreciate, just at a slightly slower pace

If you’re thinking of buying, act now before mortgage rates and home prices increase further. If you’re thinking of selling, your best bet may be to sell soon so you can beat the increase in competition that’s about to come to market.

If you’re thinking of buying a home today, you already know that the number of homes available for sale is low. But what does that really mean for you? As a buyer, low housing supply coupled with high buyer demand means you should be prepared to navigate a highly competitive market where homes sell fast and get multiple offers. Realtor.com has this to say:

“Homes also flew off the market at record pace as buyers put offers in the moment properties came up for sale….”

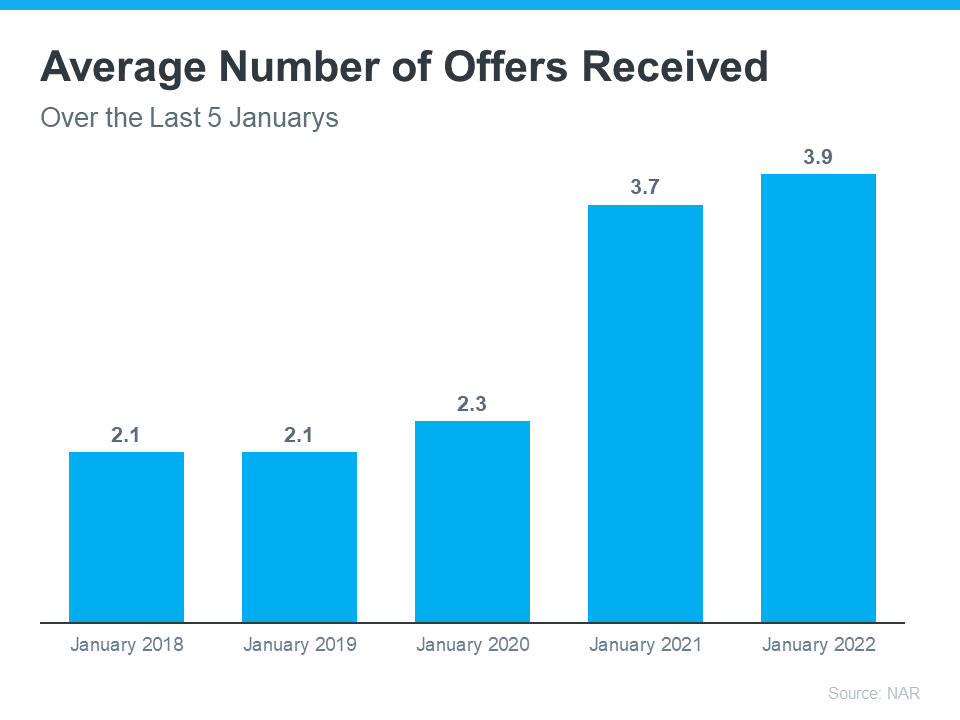

In a bidding war situation like this, doing everything you can to get ahead of the competition is a wise move. That’s because when you find a house and submit an offer, it’ll likely be up against strong offers from other buyers. According to the latest RealtorsConfidence Index from the National Association of Realtors (NAR), homes today are receiving an average of 3.9 offers. That’s the most offers we’ve seen in January for the last 5 years (see graph below):

To help you navigate bidding wars with multiple offers, an expert real estate advisor is key. They know what’s worked for other buyers, what sellers are looking for, and how to help you prepare when it comes time to make an offer. Here are three tips to keep in mind that will help you make the best offer possible.

1. Know Your Numbers

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. Pre-approval shows sellers you’re serious, which can give you a competitive edge. You should also know making an offer at the home’s asking price may not be enough. Homes today often sell for more than their listing price. An agent can help you understand the market value of the home and what other homes are selling for in your area.

2. Be Ready To Move Fast

Speed and the pace of sales are contributing factors to today’s competitive housing market. When homes are selling fast, it’s important to stay on top of the market and be ready to move quickly. Your agent will help you stay up to date on the latest listings and help you put together your best offer as soon as you find the home you want to buy.

3. Make a Strong but Fair Offer

When you’re up against other offers, putting your best offer forward from the start is key. Lean on your agent to write a strong offer and use their expertise on which levers you can pull to make your offer as enticing as possible. One option is to wave some of your contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Just remember there are certain contingencies you don’t want to give up, like the home inspection.

Bottom Line

No matter what, your agent is your best resource for making an offer that stands out in a competitive market. Let’s connect to talk through what you can expect as a buyer and how to kick off a successful home search.

As a homebuyer, it’s important to plan and budget for the expenses you’ll encounter when you purchase a home. While most people understand the need to save for a down payment, a recent survey found 41% of homebuyers were surprised by their closing costs. Here’s some information to help you get started so you’re not caught off guard when it’s time to close on your home.

What Are Closing Costs?

One possible reason some people are surprised by closing costs may be because they don’t know what they are or what they cover. According to U.S. News and World Report:

“Closing costs encompass a variety of expenses above your property’s purchase price. They include things like lender fees, title insurance, government processing fees, upfront tax payments and homeowners insurance.”

In other words, your closing costs are a collection of fees and payments made to a variety of individuals and organizations who are involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include:

Government recording costs

Appraisal fees

Credit report fees

Lender origination fees

Title services

Tax service fees

Survey fees

Attorney fees

Underwriting Fees

How Much Will You Need To Budget for Closing Costs?

Understanding what closing costs include is important, but knowing what you’ll need to budget to cover them is critical to achieving your homebuying goals. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $350,300. Based on the 2-5% Freddie Mac estimate, your closing fees could be between roughly $7,000 and $17,500.

Keep in mind, if you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

What’s the Best Way To Make Sure You’re Prepared At Closing Time?

Freddie Mac provides great advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

The best way to understand what you’ll need at the closing table is to work with a team of trusted real estate professionals. An agent can help connect you with a lender, and together they can provide you with answers to the questions you might have.

Bottom Line

In today’s real estate market, it’s more important than ever to make sure your budget includes any fees and payments due at closing. Let’s connect so you have the knowledge you need to be confident going into the homebuying process.

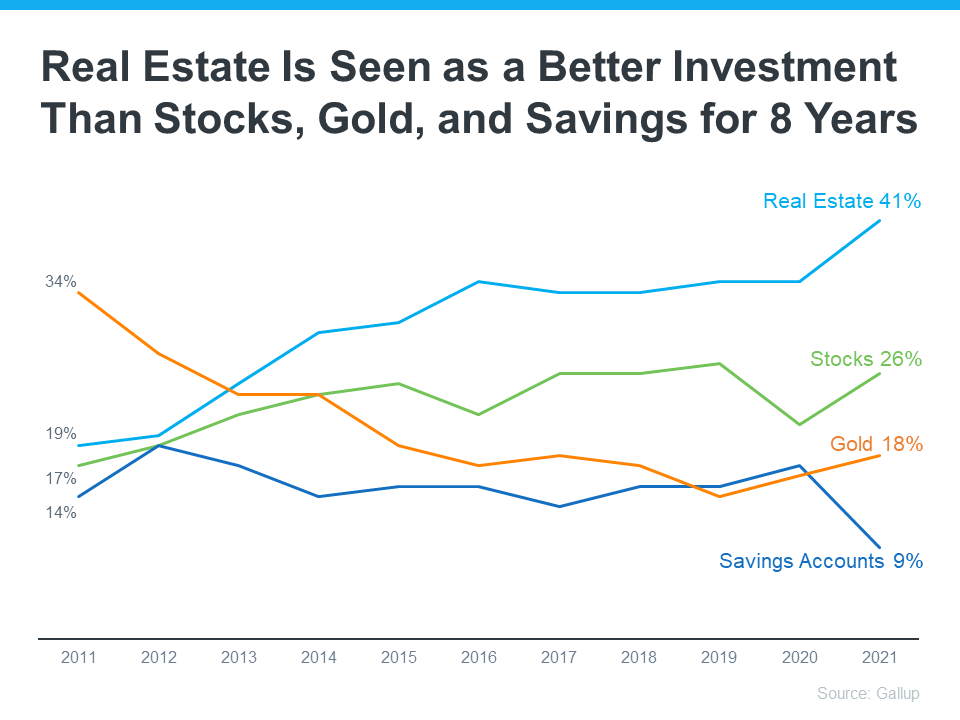

In an annual Gallup poll, Americans chose real estate as the best long-term investment. And it’s not the first time it’s topped the list, either. Real estate has been on a winning streak for the past eight years, consistently gaining traction as the best long-term investment (see graph below):

If you’re thinking about purchasing a home this year, this poll should reassure you. Even when inflation is rising like it is today, Americans agree an investment like real estate truly shines.

Why Is Real Estate a Great Investment During Times of High Inflation?

With inflation reaching its highest level in 40 years, it’s more important than ever to understand the financial benefits of homeownership. Rising inflation means prices are increasing across the board. That includes goods, services, housing costs, and more. But when you purchase your home, you lock in your monthly housing payments, effectively shielding yourself from increasing housing payments. James Royal, Senior Wealth Management Reporter at Bankrate, explains it like this:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

If you’re a renter, you don’t have that same benefit, and you aren’t protected from increases in your housing costs, especially rising rents.

History Shows During Inflationary Periods, Home Prices Rise as Well

As a homeowner, your house is an asset that typically increases in value over time, even during inflation. That‘s because, as prices rise, the value of your home does, too. And that makes buying a home a great hedge during periods of high inflation. Natalie Campisi, Advisor Staff for Forbes, notes:

“Tangible assets like real estate get more valuable over time, which makes buying a home a good way to spend your money during inflationary times.”

Bottom Line

Housing truly is a strong investment, especially when inflation is high. When you lock in a mortgage payment, you’re shielded from housing cost increases, and you own an asset that typically gains value with time. If you want to better understand how buying a home could be a great investment for you, let’s connect today.

Having an experienced guide coaching you through the process of buying or selling a home is important in a normal market – but today’s market is far from normal. As a result, an expert real estate advisor isn’t just good to have by your side, they’re essential.

Today’s housing market is full of extremes. Experts project mortgage rates will continue to rise this year, and that’s driving significant demand for homes as buyers want to make their purchases before rates climb even higher. At the same time, an absence of sellers is leading to record-low housing inventory. This imbalance in supply and demand is creating bidding wars and driving home price appreciation as well as considerable gains in home equity.

These market conditions can feel overwhelming, but you don’t have to go at it alone. Having a trusted expert to coach you through the process of buying or selling a home gives you clarity and confidence through each step.

Here are just a few of the ways a real estate expert is invaluable:

Contracts – Agents help with the disclosures and contracts necessary in today’s heavily regulated environment.

Experience – In an unprecedented market, experience is crucial. Real estate professionals know the entire sales process, including how it’s changed over the past two years.

Negotiations – Your real estate advisor acts as a buffer in negotiations with all parties throughout the entire transaction and advocates for your best interests.

Education – Knowledge is power in today’s market, and your advisor will simply and effectively explain market conditions and translate what they mean for you.

Pricing – Finally, a real estate professional understands today’s real estate values when setting the price of your home or helping you make an offer to purchase one.

A real estate agent is a crucial guide through this unprecedented market, but not all agents are created equal. A true expert can carefully walk you through the whole real estate process, look out for your unique needs, and advise you on the best ways to achieve success. Finding an expert real estate advisor – not just any agent – should be your top priority when you’re ready to buy or sell a home.

What’s the key to choosing the right expert?

It starts with trust. You’ll want to know you can trust the advice they’re giving you, so you need to make sure you’re connected with a true professional. No one can provide perfect advice because it’s impossible to know exactly what’s going to happen at every turn – especially in today’s unique market. But a true professional can give you the best possible advice based on the information and situation at hand. They’ll help you make the necessary adjustments along the way, advocate for you throughout the process, and coach you on the essential knowledge you need to make confident decisions. That’s exactly what you want and deserve.

Bottom Line

It’s critical to have an expert on your side who’s well versed in navigating today’s rapidly changing market. If you’re planning to buy or sell a home this year, let’s connect so you have a real estate professional on your side to give you the best advice and guide you along the way.

If you’re a millennial, homebuying might be top of mind for you. Your generation is the largest group of homebuyers in the market today and has been since 2014, according to the National Association of Realtors (NAR). And while other millennials are looking to buy for the first time, you may be one of the many who are now discovering you’ve outgrown your home.

If that’s the case, you’re not alone. The past two years brought about significant changes for many people, and today, homeowners are reevaluating what they truly need in a home. As a recent report from the Wall Street Journal states:

“They say the pandemic and the emergence of remote work accelerated millennial home-buying trends already under way. . . . Millennials who already owned homes traded up for more space.”

So, if you’re working remotely now or simply have a growing need for additional space, it may be time to move. And even if you purchased your current home sometime over the last few years, you can still move into a different one that has the space and features you’re looking for. That’s because there’s a good chance you have more equity than you realize. As Diana Olick, Real Estate Correspondent for CNBC, notes:

“The stunning jump in home values over the course of the Covid-19 pandemic has given U.S. homeowners record amounts of housing wealth. . . . Even homeowners who weren’t listing their properties for sale were gaining equity. About 42% of homeowners were considered equity-rich at the end of last year, meaning their mortgages were half or less than half the value of their home.”

Growing equity can be the key you need to fuel your next move, especially if you’re looking to purchase a larger home. When you sell your current house, the equity that comes back to you in the sale can be used toward the down payment on your next home.

In other words, your purchasing power may be greater than you realize, making a move to a larger home a realistic option. That, plus your changing needs, might make moving now more desirable than ever.

Bottom Line

If you’re a millennial thinking about moving this year, you’re not alone. Let’s connect today to discuss the equity you have in your current home and the opportunities it can create.

Homeownership has long been considered the American Dream, and it’s one every American should feel confident and powerful pursuing. But owning a home is also a deeply personal dream. Our home provides us with safety and security, and it’s a place where we can grow and flourish.

Today, we remember the legacy of Dr. Martin Luther King, Jr. Many of us will remember his passion and determination for the causes he championed, including his famous “I Have a Dream” speech in 1963. As we reflect on his message today, it may inspire your own dream of homeownership. And if so, know you’re not alone. With a trusted real estate advisor at your side, you can begin your journey toward homeownership by answering the questions below.

1. Where Do I Start?

The process of buying a home is not one to enter into lightly. You need to decide on key things like how long you plan on living in an area, how much space you need, what kind of commute works for you, and how much you can spend.

Then, when you decide you’re ready to buy, you’ll need to apply for a mortgage. Your lender will look at several factors to determine how much you’re able to borrow, including your credit history. Lenders want to understand how well you’ve managed paying your student loans, credit cards, car loans, and other past debts.

“To get a rough estimate of what you can afford, most lenders suggest that you should spend no more than 28% of your monthly gross (pre-tax) income on your mortgage payment, including principal, interest, taxes and insurance.”

2. How Do I Save Enough for a Down Payment?

Speaking of how much you can afford, you’ll want to know what to save for a down payment. While the idea of saving for a down payment can be daunting, there are many different options and resources that can help.

According to Business Insider, automatic savings can bring you one step closer to achieving your target down payment:

“If you receive your paycheck as a direct deposit, you may want to arrange for your company to send a percentage of each check directly into a savings account for the down payment. . . . The automatic-savings strategy makes it so you don’t have to constantly remember to save money.”

Before you know it, you’ll have enough for a down payment if you’re disciplined and thoughtful about your process. And the best part is, you may need to save less for your down payment than you think. Your agent and lender can help you understand your options.

3. How Can I Reach My Financial Goals?

Another way to increase your savings is by sticking to a planned budget. If you’ve never budgeted before, there are tools available. For example, MoneyFit.org provides a budgeting worksheet you can use to create your own plan and five rules to follow when you’re saving. They recommend you:

Identify Goals

Record Expenses

Record Earnings

Compare and Calculate

Fix Weak Spots

If you’re already budgeting, consider finding ways to tighten your spending a bit more to accelerate your journey to homeownership. After all, putting even a little extra into your savings each month can truly add up over time.

Bottom Line

As you set out to realize your dream of homeownership this year, know that it’s achievable with careful planning. Most importantly, let’s connect today so you don’t have to walk alone on this journey.