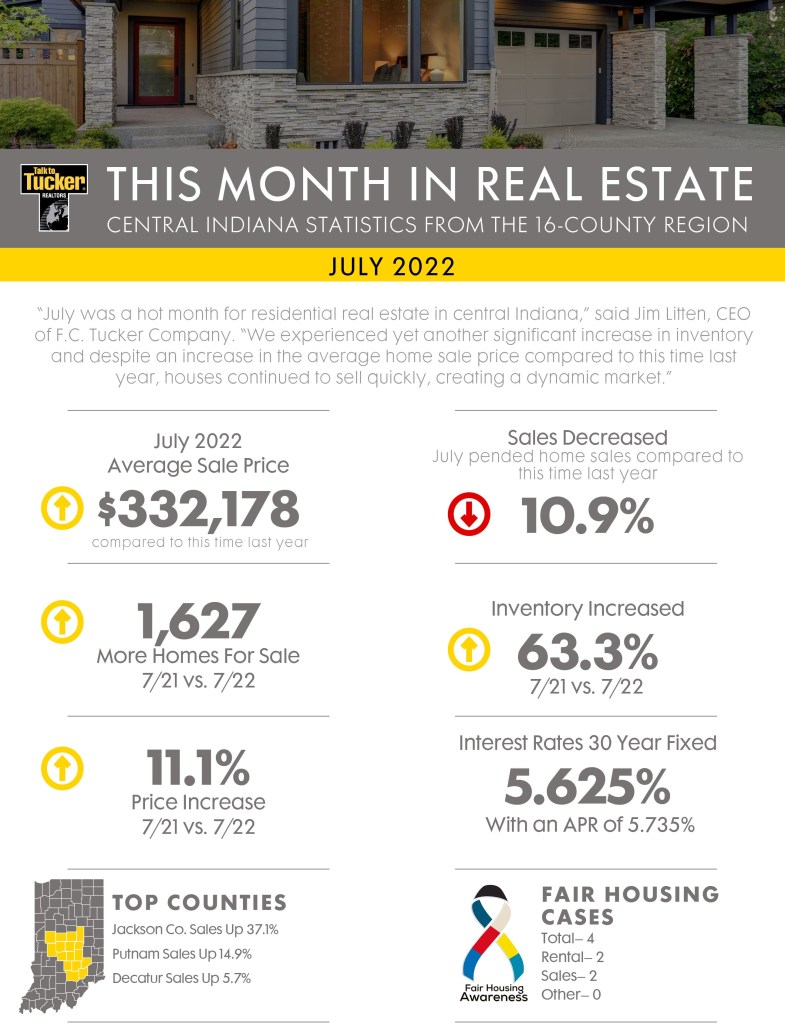

JULY 2022 MARKET UPDATE

Indianapolis Area Homes for Sale

Shawna O'Brien, Realtor/Broker Indy, Geist, Fishers, Carmel & all surrounding areas

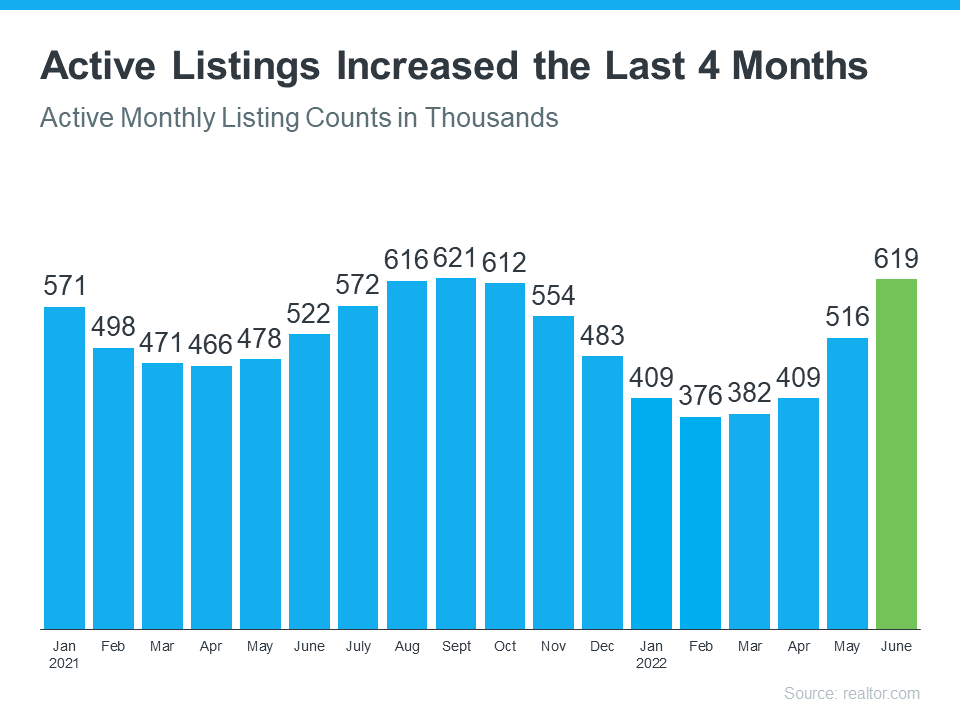

There are more homes for sale today than at any time last year. So, if you tried to buy a home last year and were outbid or out priced, now may be your opportunity. The number of homes for sale in the U.S. has been growing over the past four months as rising mortgage rates help slow the frenzy the housing market saw during the pandemic.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why the shifting market creates a window of opportunity for you:

“This is an opportunity for people with a secure job to jump into the market, when other people are a little hesitant because of a possible recession. . . They’ll have fewer buyers to compete with.”

The first reason the market is seeing more homes available for sale is the number of sales happening each month has decreased. This slowdown has been caused by rising mortgage rates and rising home prices, leading many to postpone or put off buying. The graph below uses data from realtor.com to show how active real estate listings have risen over the past four months as a result.

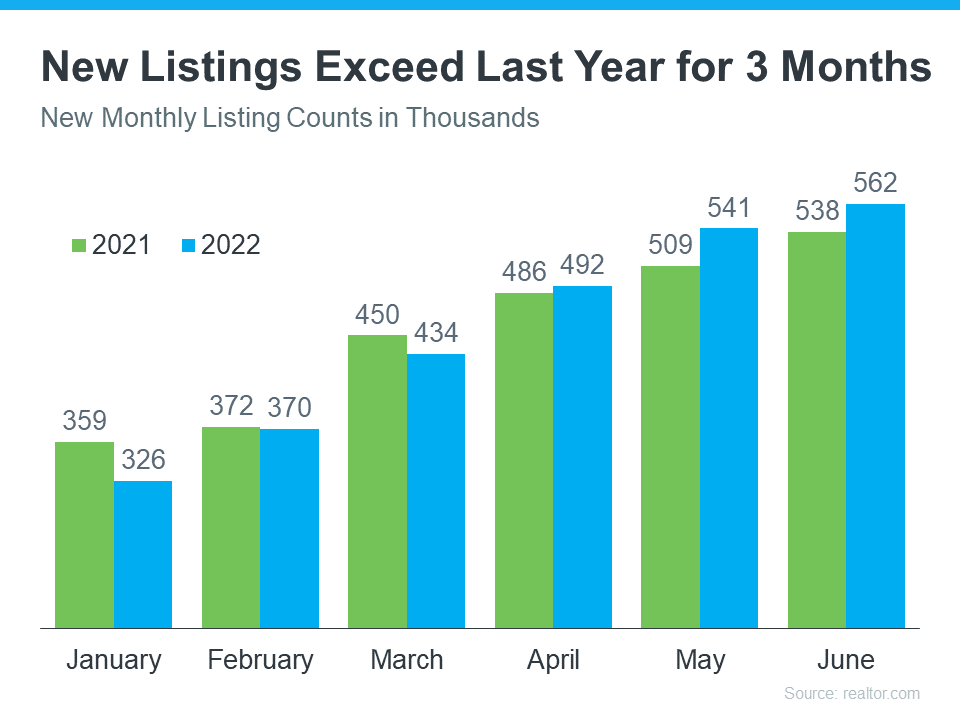

The second reason the market is seeing more homes available for sale is because the number of people selling their homes is also rising. The graph below outlines new monthly listings coming onto the market compared to last year. As the graph shows, for the past three months, more people have put their homes on the market than the previous year.

The number of homes for sale across the country is growing, and that means more options for those thinking about buying a home. This is the opportunity many have been waiting for who were outbid or out priced last year.

Shawna O’Brien

F.C. Tucker Geist Fishers

shawna.obrien@talktotucker.com

317-506-0039

According to a recent survey, more and more Americans are concerned about a possible recession. Those concerns were validated when the Federal Reserve met and confirmed they were strongly committed to bringing down inflation. And, in order to do so, they’d use their tools and influence to slow down the economy.

All of this brings up many fears and questions around how it might affect our lives, our jobs, and business overall. And one concern many Americans have is: how will this affect the housing market? We know how economic slowdowns have impacted home prices in the past, but how could this next slowdown affect real estate and the cost of financing a home?

According to Mortgage Specialists:

“Throughout history, during a recessionary period, interest rates go up at the beginning of the recession. But in order to come out of a recession, interest rates are lowered to stimulate the economy moving forward.”

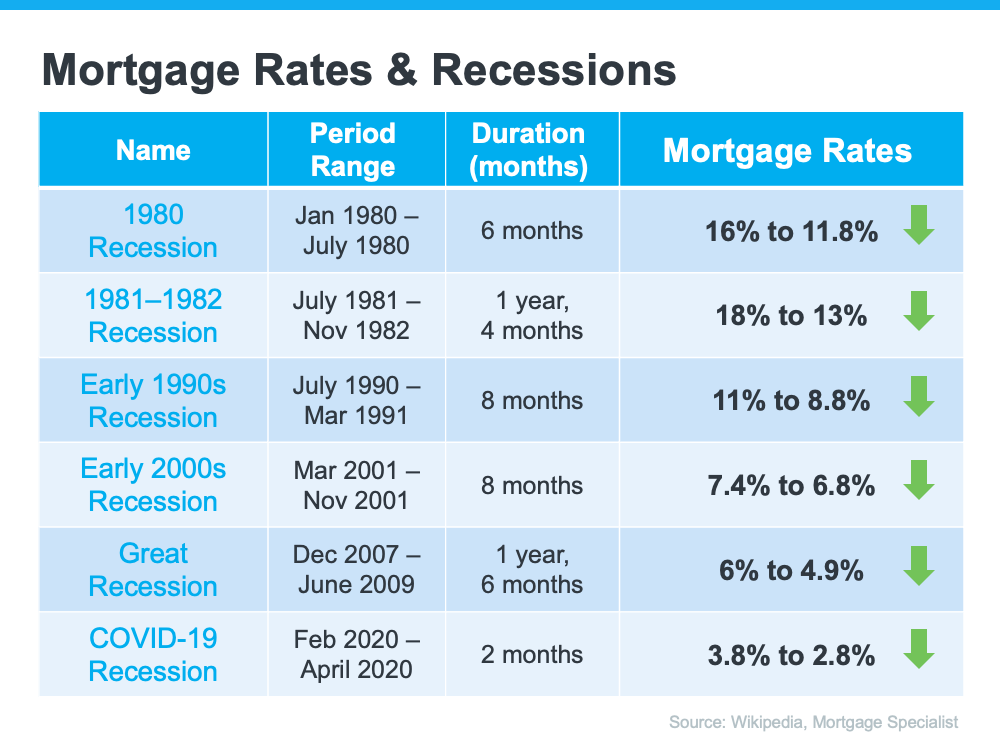

Here’s the data to back that up. If you look back at each recession going all the way to the early 1980s, here’s what happened to mortgage rates during those times (see chart below):

As the chart shows, historically, each time the economy slowed down, mortgage rates decreased. Fortune.com helps explain the trend like this:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

And while history doesn’t always repeat itself, we can learn from it. While an economic slowdown needs to happen to help taper inflation, it hasn’t always been a bad thing for the housing market. Typically, it has meant that the cost to finance a home has gone down, and that’s a good thing.

Concerns of a recession are rising. As the economy slows down, history tells us this would likely mean lower mortgage rates for those looking to refinance or buy a home. While no one knows exactly what the future holds, you can make the right decision for you by working with a trusted real estate professional to get expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Shawna O’Brien

F.C. Tucker Geist Fishers

shawna.obrien@talktotucker.com

317-506-0039

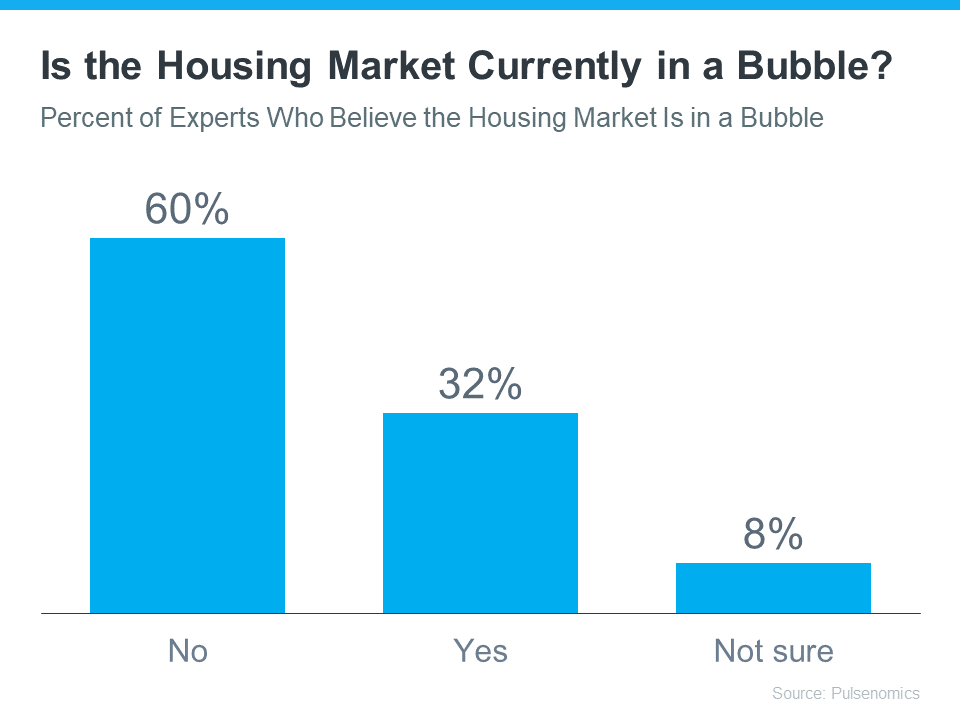

You may be reading headlines and hearing talk about a potential housing bubble or a crash, but it’s important to understand that the data and expert opinions tell a different story. A recent survey from Pulsenomics asked over one hundred housing market experts and real estate economists if they believe the housing market is in a bubble. The results indicate most experts don’t think that’s the case (see graph below):

As the graph shows, a strong majority (60%) said the real estate market is not currently in a bubble. In the same survey, experts give the following reasons why this isn’t like 2008:

If you’re concerned a crash may be coming, here’s a deep dive into those two key factors that should help ease your concerns.

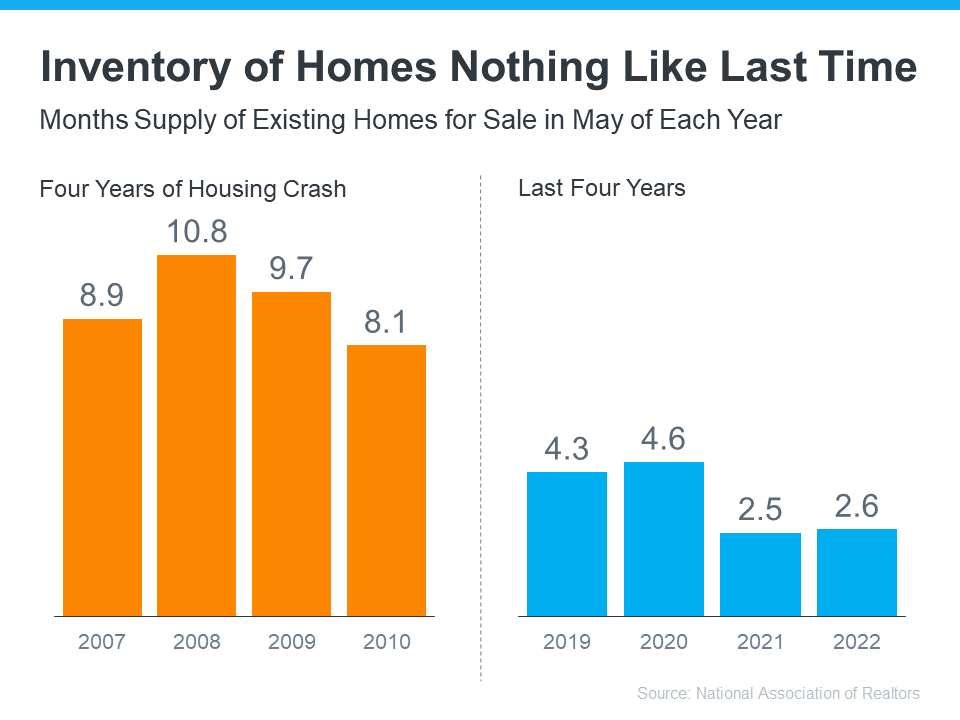

The supply of homes available for sale needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued price appreciation.

As the graph below shows, there were too many homes for sale from 2007 to 2010 (many of which were short sales and foreclosures), and that caused prices to tumble. Today, there’s still a shortage of inventory, which is causing ongoing home price appreciation (see graph below):

Inventory is nothing like the last time. Prices are rising because there’s a healthy demand for homeownership at the same time there’s a limited supply of homes for sale. Odeta Kushi, Deputy Chief Economist at First American, explains:

“The fundamentals driving house price growth in the U.S. remain intact. . . . The demand for homes continues to exceed the supply of homes for sale, which is keeping house price growth high.”

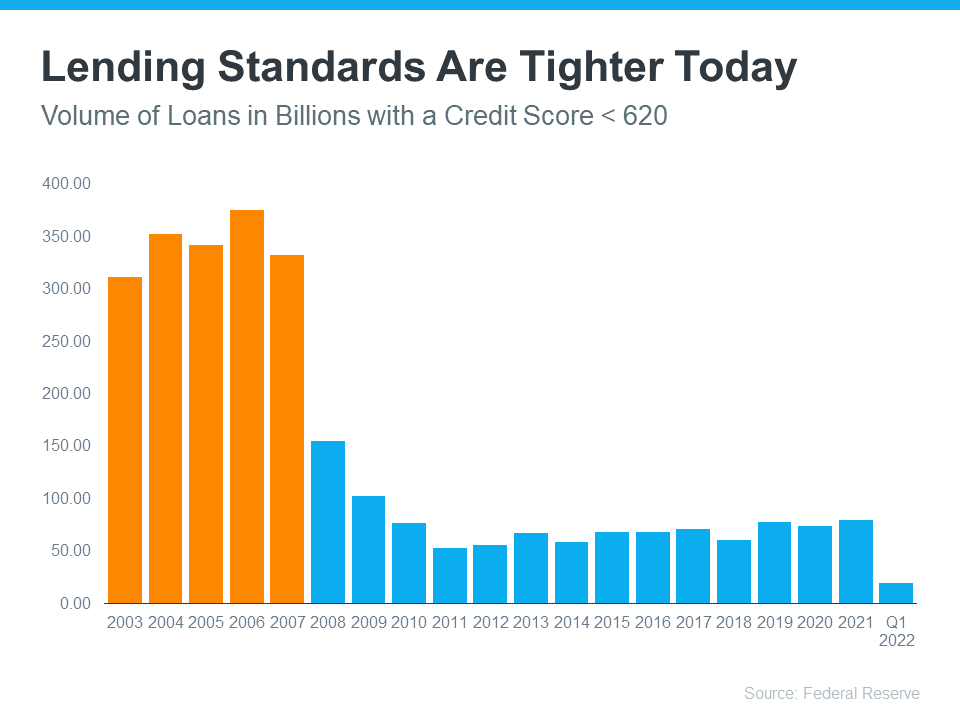

During the housing bubble, it was much easier to get a mortgage than it is today. Here’s a graph showing the mortgage volume issued to purchasers with a credit score less than 620 during the housing boom, and the subsequent volume in the years after:

This graph helps show one element of why mortgage standards are nothing like they were the last time. Purchasers who acquired a mortgage over the last decade are much more qualified than they were in the years leading up to the crash. Realtor.com notes:

“. . . Lenders are giving mortgages only to the most qualified borrowers. These buyers are less likely to wind up in foreclosure.”

Bottom Line

A majority of experts agree we’re not in a housing bubble. That’s because home price growth is backed by strong housing market fundamentals and lending standards are much tighter today. If you have questions, let’s connect to discuss why today’s housing market is nothing like 2008.

Shawna O’Brien

F.C. Tucker Geist Fishers

shawna.obrien@talktotucker.com

317-506-0039

Owning a Home in the Age of Inflation?

The housing market is already painfully tight with bidding wars breaking out all over. Now, inflation (and interest rates, right along with it) are on the rise. Just looking at the prices on property listings online has you feeling the strain on your home-buying budget.

Given that the Federal Reserve typically hikes mortgage interest rates in order to slow inflation down and the fact that you may have to compensate by settling for less house than you initially wanted, is this really a good time to buy a home?

It could be. In fact, it could be far better to buy today than to wait. Here are all the things you need to know before you decide if homeownership is really in the cards for you:

Why You Shouldn’t Let Inflation Worries Keep You From Buying

First, you need to keep in mind that sage advice about how “the best time to buy a house is always five years ago,” because housing prices tend to keep increasing over time. There are no major indications that we’re in a real estate “bubble” that will simply collapse in the near future and lower the prices dramatically, either. The issues that gave rise to the real estate bust of 2008 simply aren’t in the picture today.

Second, real estate is typically seen as a good way to hedge against rising inflation. If you continue renting, your rent isn’t going to go down because inflation is rising. In fact, your rent is likely to increase. If you lock in a reasonable interest rate now on a fixed-rate mortgage, you have the security of knowing that your monthly payment will remain predictable while other costs are soaring.

Finally, putting your money into a mortgage helps you build wealth in three different ways:

1. You start building equity: When you rent, every dollar you pay goes into your landlord’s pocket, not yours. With a mortgage, you’re putting money back into your pocket each month in the form of equity in your home.

2. You raise your net worth: Despite occasional dips in the market, a well-maintained home is only likely to rise in value over time. As its value rises, so does your net worth. That gives you far more room to access funds for other needs in the future, like your child’s education or renovations.

3. You gain a significant tax break: The interest on your mortgage and your property taxes are both significant tax breaks. That can help you keep more of your money to pour into everything from your emergency fund to vacations.

It’s also important to remember that mortgage rates still are fairly low. Still plenty low enough to make mortgages attractive to most buyers — and plenty low enough to make a mortgage preferable to a rental payment.

Waiting to buy, however, means gambling that inflation will fall, and there’s no sign that will happen any time soon.

What Else You Need to Consider About Home Ownership and Inflation

When inflation is soaring, you need to remember one critical thing about owning a home: Everything you want to do in the way of renovations and everything you need to do in the way of repairs are going to cost more.

Supply chain issues and rising fuel costs have already driven up prices on all kinds of building materials, so you need to keep that in mind when you’re viewing homes for sale. A fixer-upper may not be a big deal if you’re handy, but the cost of your supplies could be outrageous right now. For that reason, you may want to steer clear of homes that look like they need major updates.

When you are thinking about renovations, you want to make every dollar count. Put your money into the repairs and upgrades that are most economically sound and meaningful. That may mean prioritizing a new roof over stainless steel appliances for the kitchen or adding a home office instead of an extra half-bath on the main floor.

Finally, you also need to keep your overall budget in mind. Inflation is bound to lead to increases in things like:

• Moving costs

• Repair fees

• Utilities

• Grocery bills

• Homeowners association dues

• Insurance costs

One of the wisest things you can do when you’re looking ahead to the cost of homeownership is to make sure that you have enough money set aside — after you make your down payment on a home and pay for any essentials — to cover anywhere from six to 12 months’ worth of expenses.

Shawna O’Brien

F.C. Tucker Geist Fishers

shawna.obrien@talktotucker.com

317-506-0039

If you’re following the news, all of the headlines about conditions in the current housing market may leave you with more questions than answers. Is the boom over? Is the market crashing or correcting? Here’s what you need to know.

The housing market is moderating compared to the last two years, but what everyone needs to remember is that the past two years were record-breaking in nearly every way. Record-low mortgage rates and millennials reaching peak homebuying years led to an influx of buyer demand. At the same time, there weren’t enough homes available to purchase thanks to many years of underbuilding and sellers who held off on listing their homes due to the health crisis.

This combination led to record-high demand and record-low supply, and that wasn’t going to be sustainable for the long term. The latest data shows early signs of a shift back to the market pace seen in the years leading up to the pandemic – not a crash nor a correction. As realtor.com says:

“The housing market is at a turning point. . . . We’re starting to see signs of a new direction, . . .”

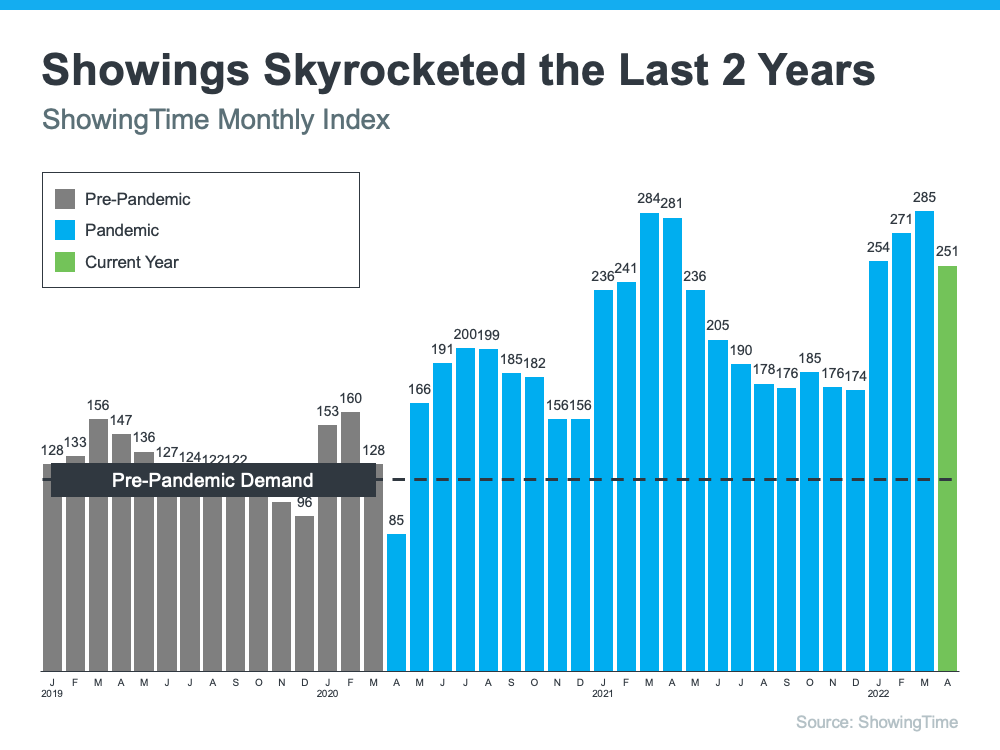

The ShowingTime Showing Index tracks the traffic of home showings according to agents and brokers. It’s a good indication of buyer demand. Here’s a look at that data going back to 2019 (see graph below):

The 2019 numbers give a good baseline of pre-pandemic demand (shown in gray). As the graph indicates, home showings skyrocketed during the pandemic (shown in blue). And while current buyer demand has begun to moderate slightly based on the latest data (shown in green), showings are still above 2019 levels.

And since 2019 was such a strong year for the housing market, this helps show that the market isn’t crashing – it’s just at a turning point that’s moving back toward more pre-pandemic levels.

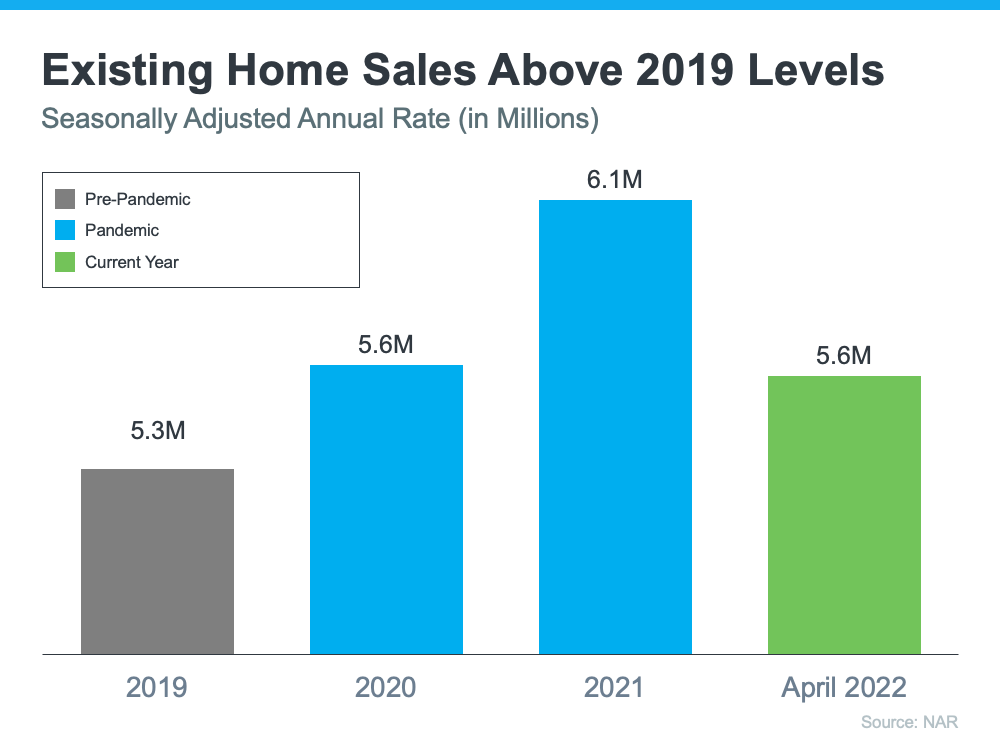

Headlines are also talking about how existing home sales are declining, but perspective matters. Here’s a look at existing home sales going all the way back to 2019 using data from the National Association of Realtors (NAR) (see graph below):

Again, a similar story emerges. The pandemic numbers (shown in blue) beat the more typical year of 2019 home sales (shown in gray). And according to the latest projections for 2022 (shown in green), the market is on pace to close this year with more home sales than 2019 as well.

It’s important to compare today not to the abnormal pandemic years, but to the most recent normal year to show the current housing market is still strong. First American sums it up like this:

“. . . today’s housing market looks a lot like the 2019 housing market, which was the strongest housing market in a decade at the time.”

If recent headlines are generating any concerns, look at a more typical year for perspective. The current market is not a crash or correction. It’s just a turning point toward more typical, pre-pandemic levels. Let’s connect if you have any questions about our local market and what it means for you when you buy or sell this year.

Shawna O’Brien

F.C. Tucker Geist Fishers

shawna.obrien@talktotucker.com

317-506-0039

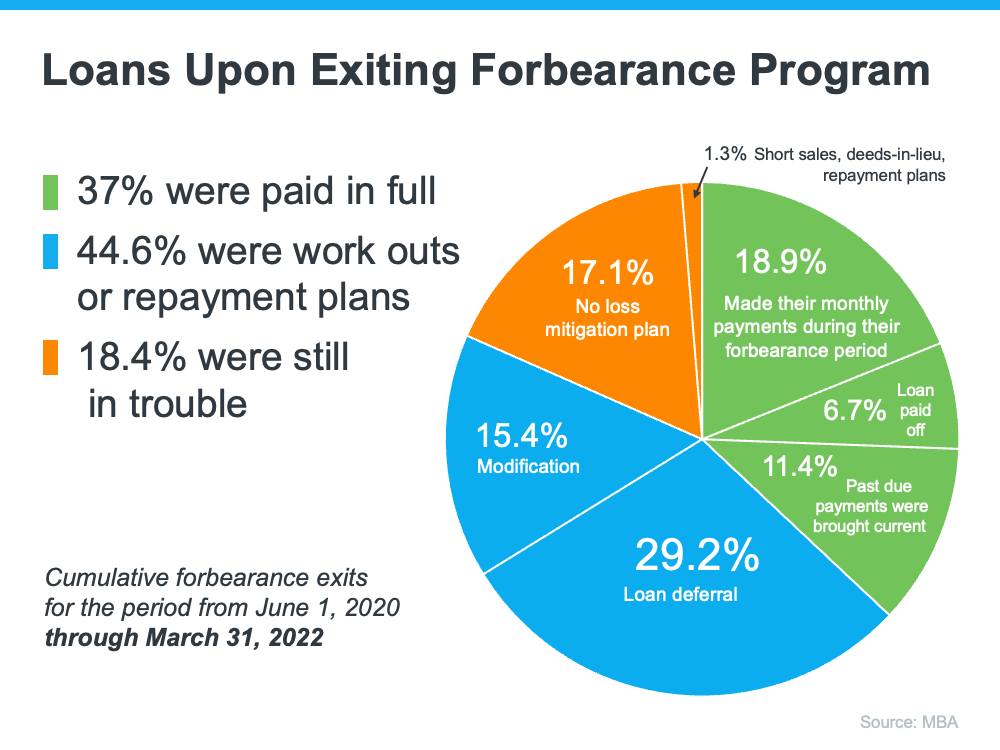

While you may have seen recent stories about the volume of foreclosures today, context is important. During the pandemic, many homeowners were able to pause their mortgage payments using the forbearance program. The goal was to help homeowners financially during the uncertainty created by the health crisis.

When the forbearance program began, many experts were concerned it would result in a wave of foreclosures coming to the market, as there was after the housing crash in 2008. Here’s a look at why the number of foreclosures we’re seeing today is nothing like the last time.

Today’s data shows that most homeowners are exiting their forbearance plan either fully caught up on payments or with a plan from the bank that restructured their loan in a way that allowed them to start making payments again. The graph below depicts those findings from the Mortgage Bankers Association (MBA):

The same MBA report mentioned above estimates there are approximately 525,000 homeowners who remain in forbearance today. Thankfully, those people still have the chance to work out a suitable repayment plan with the servicing company that represents their lender.

For those who are exiting the forbearance program without a plan in place, many will have enough equity to sell their homes instead of facing foreclosures. Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home.

Marina Walsh, CMB, Vice President of Industry Analysis at MBA, says:

“Given the nation’s limited housing inventory and the variety of home retention and foreclosure alternatives on the table across various loan types, . . . Borrowers have more choices today to either stay in their homes or sell without resorting to a foreclosure.”

One of the seldom-reported benefits of the forbearance program was it gave homeowners facing difficulties an extra two years to get their finances in order and work out a plan with their lender. That helped prevent the foreclosures that normally would have come to the market had the new forbearance program not been available.

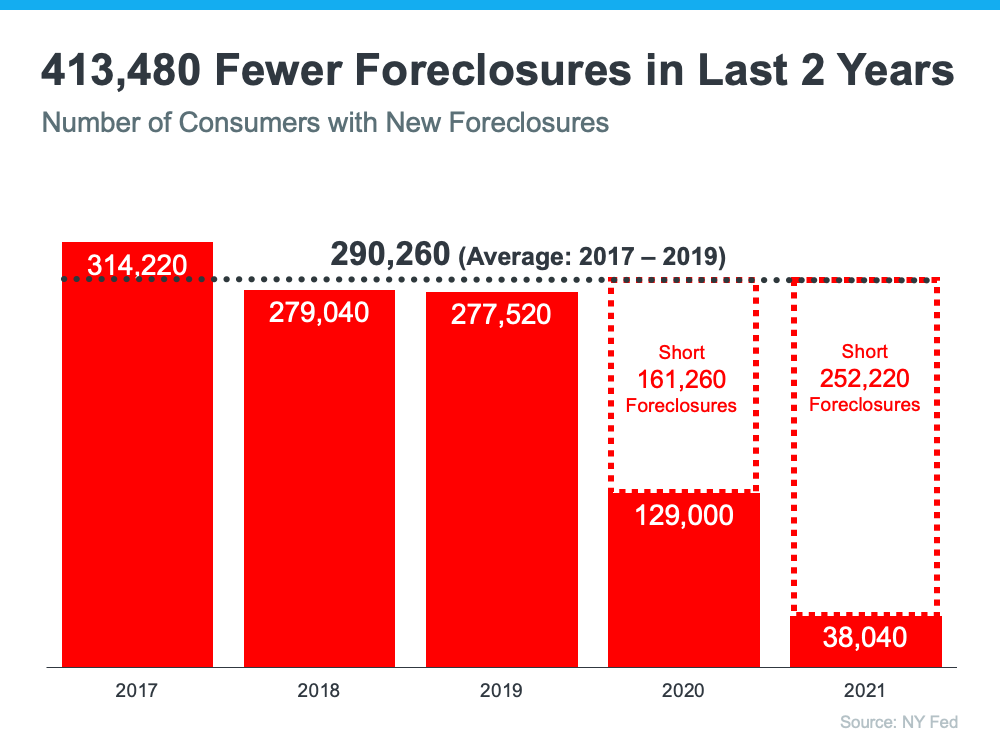

Even as people leave the forbearance program, there are still fewer foreclosures happening today than before the pandemic. That means, while there are more foreclosures now compared to last year (when foreclosures were paused), the number is still well below what the housing market has seen in a more typical year, like 2017-2019 (see graph below):

When the foreclosures in 2008 hit the market, they added to the oversupply of houses that were already for sale. It’s exactly the opposite today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) reveals:

“Total housing inventory at the end of March totaled 950,000 units, up 11.8% from February and down 9.5% from one year ago (1.05 million). Unsold inventory sits at a 2.0-month supply at the present sales pace, up from 1.7 months in February and down from 2.1 months in March 2021.”

A balanced market would have approximately a six-month supply of inventory. At 2.0 months, today’s housing market is severely understocked. Even if one million homes enter the market, there still won’t be enough inventory to meet the current demand.

If you see headlines about the increasing number of foreclosures today, remember context is important. While it’s true the number of foreclosures is higher now than it was last year, foreclosures are still well below pre-pandemic years.

If you have questions, let’s connect to talk through the latest market conditions and what they mean for you.

Shawna O’Brien

F.C. Tucker Geist Fishers

shawna.obrien@talktotucker.com

317-506-0039