Are you thinking of buying a home this summer? If so, you have a great opportunity in front of you. Here are just a few reasons why this season may be the right time to make your purchase.

1. Homeownership Has Many Perks Homeownership is the American dream – not just because it has tangible financial benefits, but because it also has the power to change lives.

2. More Homes Are Expected To Enter the Market This Summer If you begin your search now and work with a trusted real estate advisor, you’ll be in a great spot to benefit from those additional choices when your dream home hits the market.

3. Home Prices Are Climbing

4. Rents Are Rising Too To escape rising rents, consider purchasing a home so you can lock in your monthly mortgage payment.

If you’ve been thinking about buying a home, you likely have one question on the top of your mind: should I buy right now, or should I wait? While no one can answer that question for you, here’s some information that could help you make your decision.

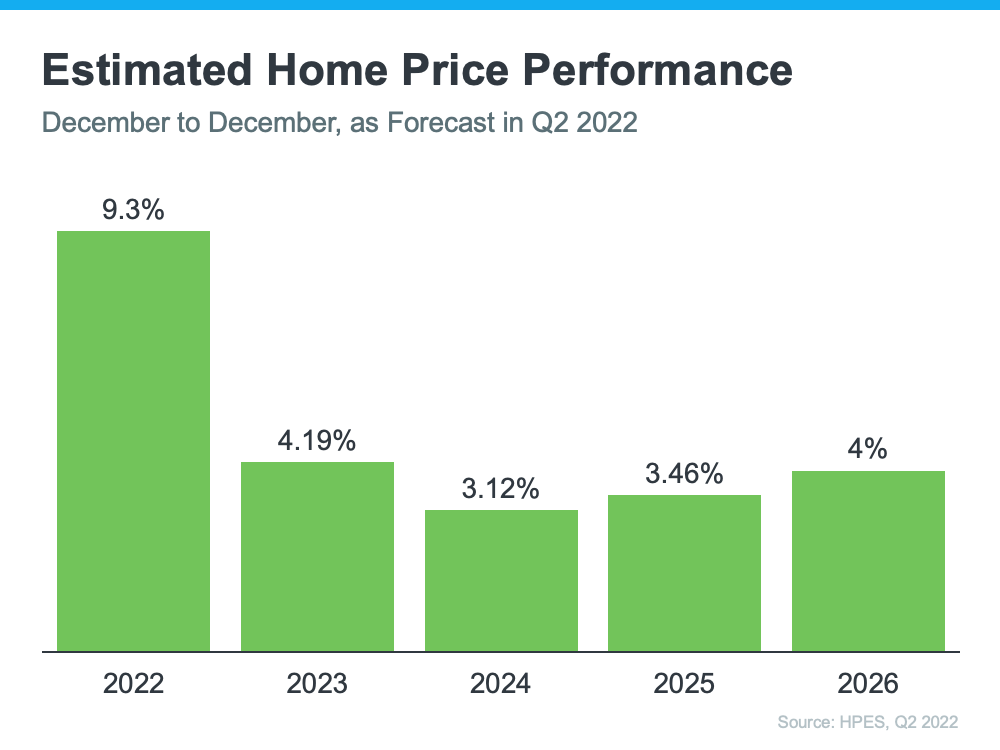

The Future of Home Price Appreciation

Each quarter, Pulsenomics surveys a national panel of over 100 economists, real estate experts, and investment and market strategists to compile projections for the future of home price appreciation. The output is the Home Price Expectation Survey. In the latest release, it forecasts home prices will continue appreciating over the next five years (see graph below):

As the graph shows, the rate of appreciation will moderate over the next few years as the market shifts away from the unsustainable pace it saw during the pandemic. After this year, experts project home price appreciation will continue, but at levels that are more typical for the market. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“People should not anticipate another double-digit price appreciation. Those days are over. . . .We may return to more normal price appreciation of 4%, 5% a year.”

For you, that ongoing appreciation should give you peace of mind your investment in homeownership is worthwhile because you’re buying an asset that’s projected to grow in value in the years ahead.

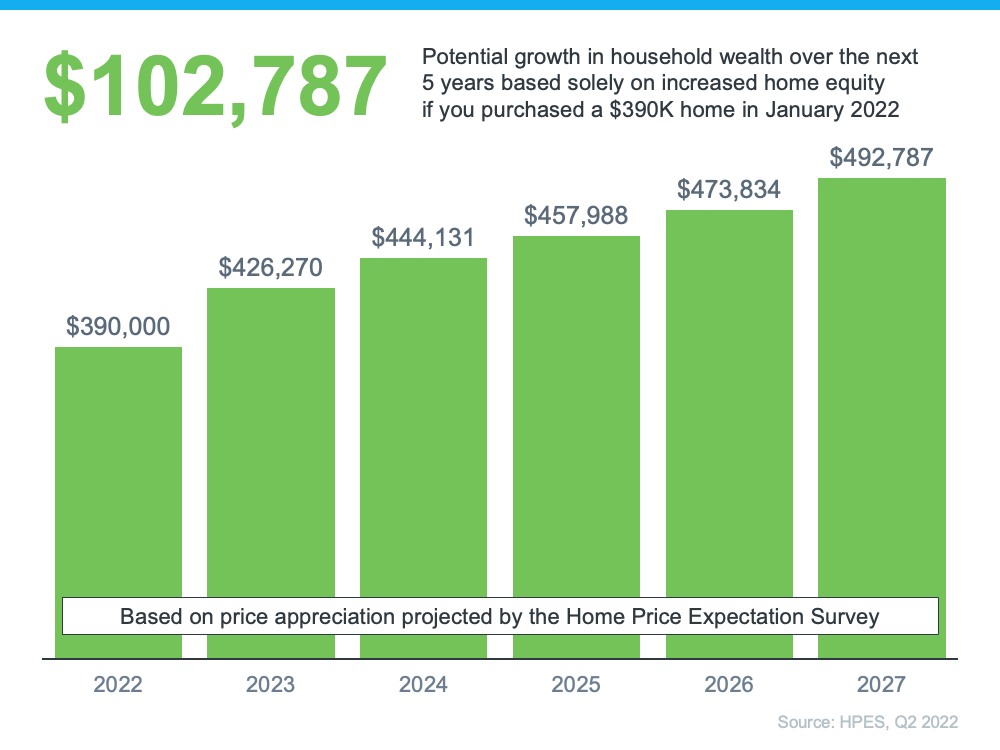

What Does That Mean for You?

To give you an idea of how this could impact your net worth, here’s how a typical home could grow in value over the next few years using the expert price appreciation projections from the Pulsenomics survey mentioned above (see graph below):

As the graph conveys, even at a more typical pace of appreciation, you still stand to make significant equity gains as your home grows in value. That’s what’s at stake if you delay your plans.

Bottom Line

If you’re ready to become a homeowner, know that buying today can set you up for long-term success as your asset’s value (and your own net worth) is projected to grow with the ongoing home price appreciation. Let’s connect to begin your homebuying process today.

It’s true that record levels of home price appreciation have spurred significant equity gains for homeowners over the past few years. As Diana Olick, Real Estate Correspondent at CNBC, says:

“The stunning jump in home values over the course of the Covid-19 pandemic has given U.S. homeowners record amounts of housing wealth.”

That’s great for your home’s value over the last couple of years, but what if you’ve lived in your home for longer than that? You may be wondering how much equity you truly have.

The National Association of Realtors (NAR) has done a study to calculate the typical equity gains over longer spans of time. The data they compiled could be enough to motivate you to move. Just remember, to find out how much equity you have in your specific home, you’ll want to get a professional equity assessment from a trusted real estate advisor.

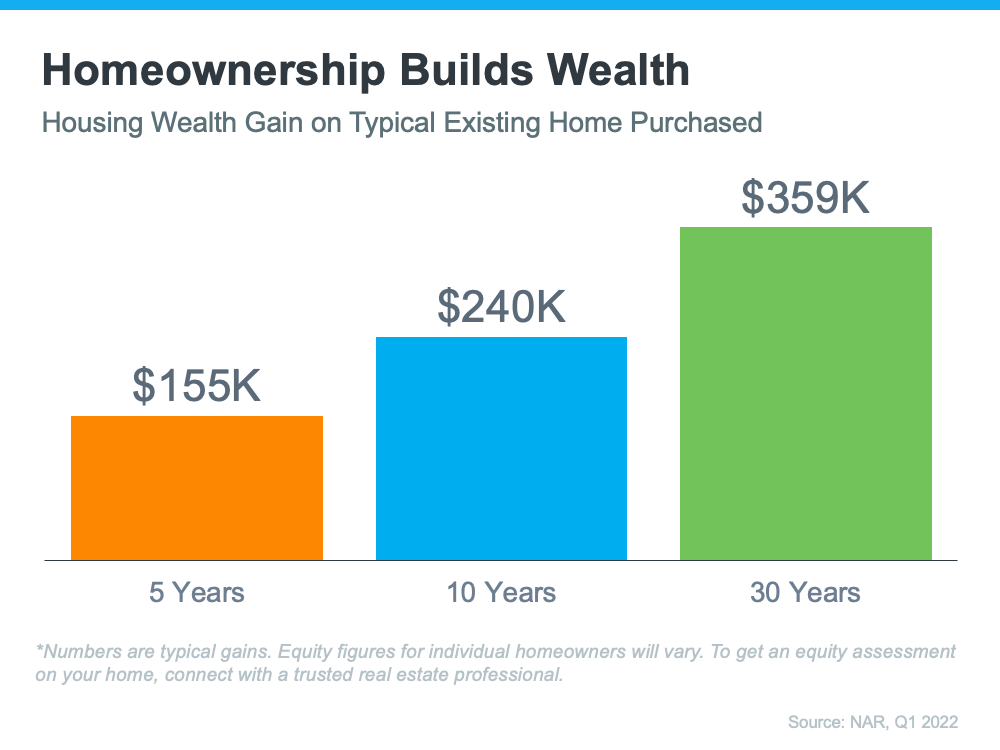

How Your Equity Grows

Let’s start by establishing how you build equity in your home. While price appreciation is clearly a factor that can help boost your equity, you also build equity over time as you pay down your home loan. NAR explains:

“Home equity gains are built up through price appreciation and by paying off the mortgage through principal payments.”

Average Equity Growth over Time

The study from NAR breaks down the typical equity gain over time (see graph below). It calculates the equity a homeowner potentially gained if they purchased the median-priced home 5, 10, or 30 years ago and still own it today.

These six-figure numbers are impressive and certainly enough to help you fuel a move into your next home, but they’re not a promised amount. Remember, your own equity gain will be different. It depends on how long you’ve been in the house, your home’s condition, any upgrades you’ve made, your area, and much more.

If you want to find out how much equity you have, partner with a trusted real estate professional for an equity assessment on your home. They can provide an expert opinion on what your house is worth today and how the equity you’ve gained over time can help you when you purchase your next home. It may be some (if not all) of what you need for your next down payment.

Bottom Line

If you’re thinking about selling your house and making a move, home equity can be a real game-changer, especially if you’ve been in your current home for a while. If you’re ready to find out how much equity you have, let’s connect.

The housing market is already painfully tight with bidding wars breaking out all over. Now, inflation (and interest rates, right along with it) are on the rise. Just looking at the prices on property listings online has you feeling the strain on your home-buying budget.

Given that the Federal Reserve typically hikes mortgage interest rates in order to slow inflation down and the fact that you may have to compensate by settling for less house than you initially wanted, is this really a good time to buy a home?

It could be. In fact, it could be far better to buy today than to wait. Here are all the things you need to know before you decide if homeownership is really in the cards for you:

Why You Shouldn’t Let Inflation Worries Keep You From Buying

First, you need to keep in mind that sage advice about how “the best time to buy a house is always five years ago,” because housing prices tend to keep increasing over time. There are no major indications that we’re in a real estate “bubble” that will simply collapse in the near future and lower the prices dramatically, either. The issues that gave rise to the real estate bust of 2008 simply aren’t in the picture today.

Second, real estate is typically seen as a good way to hedge against rising inflation. If you continue renting, your rent isn’t going to go down because inflation is rising. In fact, your rent is likely to increase. If you lock in a reasonable interest rate now on a fixed-rate mortgage, you have the security of knowing that your monthly payment will remain predictable while other costs are soaring.

Finally, putting your money into a mortgage helps you build wealth in three different ways:

1. You start building equity: When you rent, every dollar you pay goes into your landlord’s pocket, not yours. With a mortgage, you’re putting money back into your pocket each month in the form of equity in your home.

2. You raise your net worth: Despite occasional dips in the market, a well-maintained home is only likely to rise in value over time. As its value rises, so does your net worth. That gives you far more room to access funds for other needs in the future, like your child’s education or renovations.

3. You gain a significant tax break: The interest on your mortgage and your property taxes are both significant tax breaks. That can help you keep more of your money to pour into everything from your emergency fund to vacations.

It’s also important to remember that mortgage rates still are fairly low. Still plenty low enough to make mortgages attractive to most buyers — and plenty low enough to make a mortgage preferable to a rental payment.

Waiting to buy, however, means gambling that inflation will fall, and there’s no sign that will happen any time soon.

What Else You Need to Consider About Home Ownership and Inflation

When inflation is soaring, you need to remember one critical thing about owning a home: Everything you want to do in the way of renovations and everything you need to do in the way of repairs are going to cost more.

Supply chain issues and rising fuel costs have already driven up prices on all kinds of building materials, so you need to keep that in mind when you’re viewing homes for sale. A fixer-upper may not be a big deal if you’re handy, but the cost of your supplies could be outrageous right now. For that reason, you may want to steer clear of homes that look like they need major updates.

When you are thinking about renovations, you want to make every dollar count. Put your money into the repairs and upgrades that are most economically sound and meaningful. That may mean prioritizing a new roof over stainless steel appliances for the kitchen or adding a home office instead of an extra half-bath on the main floor.

Finally, you also need to keep your overall budget in mind. Inflation is bound to lead to increases in things like:

• Moving costs

• Repair fees

• Utilities

• Grocery bills

• Homeowners association dues

• Insurance costs

One of the wisest things you can do when you’re looking ahead to the cost of homeownership is to make sure that you have enough money set aside — after you make your down payment on a home and pay for any essentials — to cover anywhere from six to 12 months’ worth of expenses.

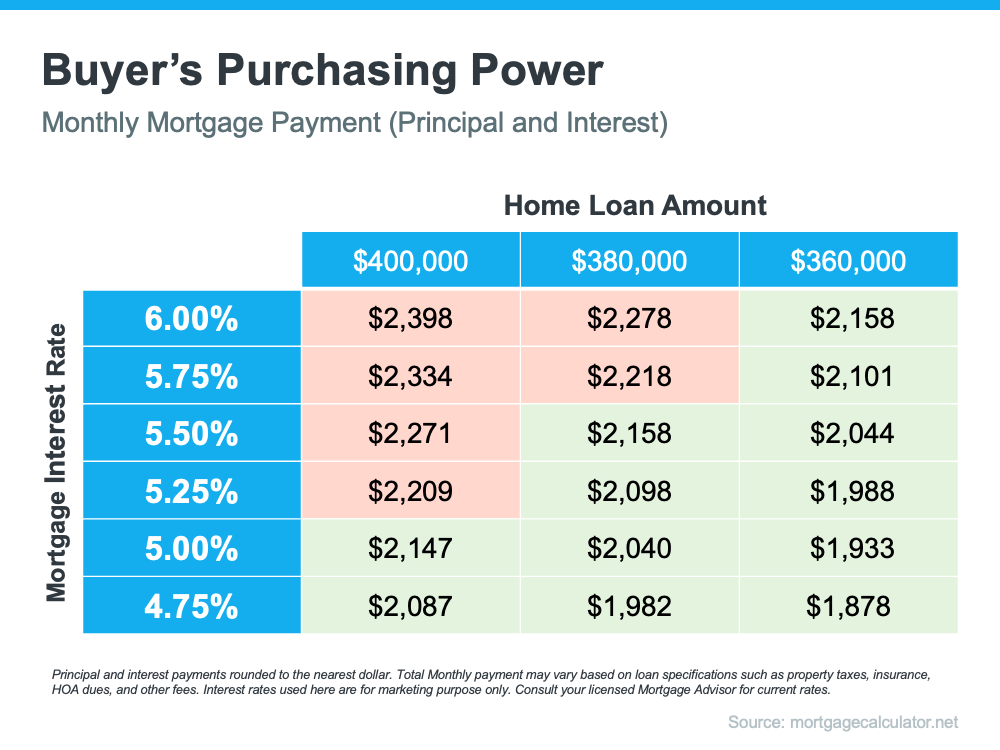

If you’re planning to buy a home, it’s critical to understand the relationship between mortgage rates and your purchasing power. Purchasing power is the amount of home you can afford to buy that’s within your financial reach. Mortgage rates directly impact the monthly payment you’ll have on the home you purchase. So, when rates rise, so does the monthly payment you’re able to lock in on your home loan. In a rising-rate environment like we’re in today, that could limit your future purchasing power.

Today, the average 30-year fixed mortgage rate is above 5%, and in the near term, experts say that’ll likely go up in the months ahead. You have the opportunity to get ahead of that increase if you buy now before that impacts your purchasing power.

Mortgage Rates Play a Large Role in Your Home Search

The chart below can help you understand the general relationship between mortgage rates and a typical monthly mortgage payment within a range of loan amounts. Let’s say your budget allows for a monthly mortgage payment in the $2,100-$2,200 range. The green in the chart indicates a payment within that range, while the red is a payment that exceeds it (see chart below):

As the chart shows, you’re more likely to exceed your target payment range as mortgage rates increase unless you pursue a lower home loan amount. If you’re ready to buy a home, use this as your motivation to purchase now so you can get ahead of rising rates before you have to make the decision to decrease what you borrow in order to stay comfortably within your budget.

Work with Trusted Advisors To Know Your Budget and Make a Plan

It’s critical to keep your budget top of mind as you’re searching for a home. Danielle Hale, Chief Economist at realtor.com, puts it best, advising that buyers should:

“Get preapproved with where rates are today, but also consider what would happen if rates were to go up, say another quarter of a point, . . . Know what that would do to your monthly costs and how comfortable you are with that, so that if rates do move higher, you already know how you need to adjust in response.”

No matter what, the best strategy is to work with your real estate advisor and a trusted lender to create a plan that takes rising mortgage rates into consideration. Together, you can look at your budget based on where rates are today and craft a strategy so you’re ready to adjust as rates change.

Bottom Line

Even small increases in mortgage rates can impact your purchasing power. If you’re in the process of buying a home, it’s more important than ever to have a strong plan. Let’s connect so you have a trusted real estate advisor and a lender on your side who can help you strategize to achieve your dream of homeownership this season.

Buying your first home is a major decision and an exciting milestone. Even though it can feel daunting at times, it has the power to change your life for the better. If you’re looking to purchase your first home, you may be wondering what’s happening in the housing market today, how much you need to save, and where to start.

Here are three things that can help give you the information you need to confidently pursue your dream of homeownership.

1. Consider All Options When the Number of Homes for Sale Is Low

Today, there are far more buyers in the market than there are homes available for sale. When that happens, it’s a good idea to do what you can to increase your pool of options. That could mean expanding your search to include additional housing types. For first-time buyers, considering condominiums (condos) and townhomes can be an excellent way to increase your choices. According to Bankrate:

“Townhomes often cost less than single-family homes of a similar size in the same location.”

“Buying a condo can be a great way to dive into homeownership without worrying about the upkeep that comes with single-family homes and townhouses.”

Condos and townhomes are both great entryways into homeownership. When you buy either one, you can start building equity which increases your net worth and can fuel a future move.

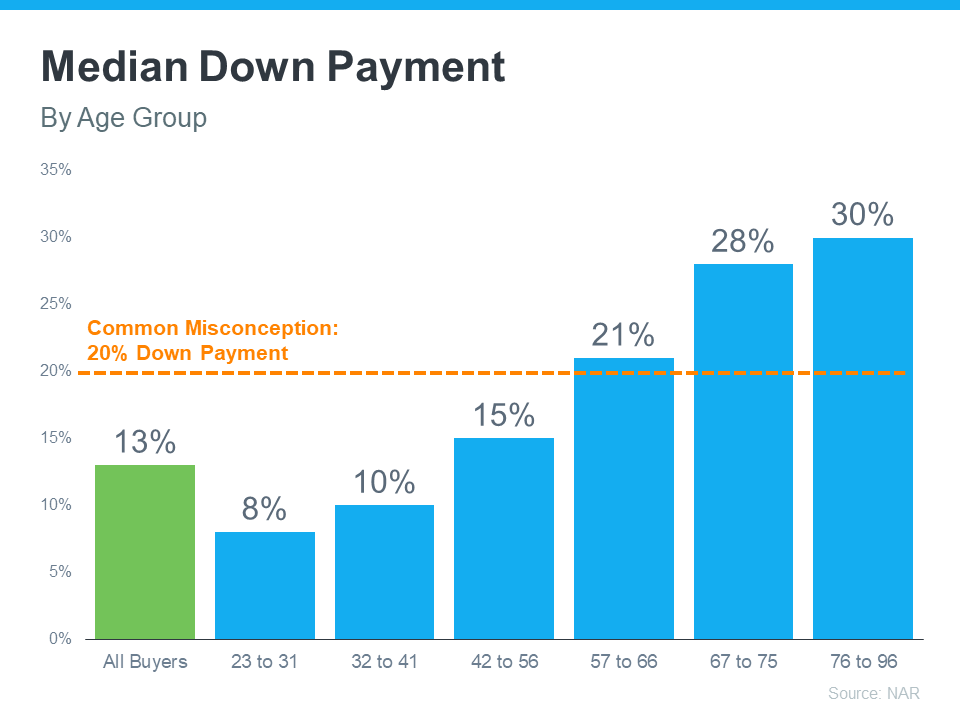

2. Know Your Down Payment Could Be More Within Reach Than You Think

Saving for a down payment can feel like one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As the National Association of Realtors (NAR) says:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership.”

Based on the data above, the median down payment for all homebuyers is only 13%. That’s well below the common misconception of 20%, and it’s even lower for younger buyers. This could mean you may not need to save as much for a down payment as you initially thought.

There are also down payment assistance programs available for many buyers. Not to mention, some loan options require as little as 3.5% (or even 0%) down for buyers who qualify. While there are advantages to putting 20% down, especially in today’s competitive market, know that you have options. To get more information on how much you may need to save and the help that’s available, talk with a professional.

3. Work with a Trusted Real Estate Advisor Throughout the Process

Finally, no matter where you’re at in your homeownership journey, the best way to make sure you’re set up for success is to work with a real estate professional.

If you’re just starting out, they can help you with the initial steps, like educating you on the process and connecting you with a trusted lender to get pre-approved. Once you’re ready to begin your search, a real estate professional can help you understand your local market and search for available homes. And when it’s time to make an offer, they’ll be an expert advisor and negotiator to help your offer stand out above the rest.

Bottom Line

Knowledge is key to succeeding on your homebuying journey. Knowing market trends, what you need for a down payment, and what options you have as a buyer today can give you the confidence you need to buy a home. Let’s connect so you have an expert on your side who can help you navigate the homebuying process.

If you’re in the market to buy a home this season, stick with it. Homebuyers face challenges in any market, and today’s is no exception. But if you persevere, your decision to purchase a home will be worth the effort in the end. In fact, a recent survey from Bankrate shows homeownership is so powerful that:

“Nearly three in four homeowners say they would still buy their current home if they had it to do [sic] all over again.”

That means the results – owning a home and the benefits that come with it – outweigh the effort needed to achieve their goal. If you’re a homebuyer, let that provide you with the confidence to know the work you’re putting in today will pay off for years to come. Here are a few reasons to stick with your search and focus on the outcome.

Homeownership Contributes Significantly to Your Financial Well-Being

“Money paid for rent is money that you’ll never see again, but mortgage payments let you build equity . . . Building equity in your home is a ready-made savings plan.”

Your equity is a powerful tool you can leverage in a number of ways. And with recent home price appreciation, homeowners are seeing record levels of equity today. That may be one reason why so many people view owning a home as a great investment and a top indicator of financial well-being. As the survey from Bankrate mentioned above shows:

“. . . Americans place a higher value on homeownership than on any other indicator of economic stability, . . .”

Owning a home ranks above other major accomplishments like retirement, having a successful career, and getting a college degree. That indicates just how impactful the financial benefits of homeownership truly are.

The Emotional Benefits of Owning a Home Are Powerful

Of course, homeownership is more than an investment. In their list of top reasons to buy a home, NAR also highlights some of the powerful, non-financial aspects of homeownership. Among them is the opportunity to customize your home to reflect your personality and needs. As they say:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Another benefit homeowners enjoy is the stability it provides. Homeowners typically stay put longer than renters. According to NAR, when you remain in one place longer than a few years, you can grow closer to your community. And that can enhance your sense of pride and lead to better relationships.

What Does That Mean for You?

The benefits of homeownership are powerful, as Leslie Rouda Smith, President of NAR, says:

“From building personal wealth and fostering communities, to strengthening social stability and driving the national economy, the value of homeownership is indisputable.”

Even if you face challenges in today’s market, the payoff when you succeed and purchase a home will be worth it.

Bottom Line

If you’re planning to buy a home this year, there are incredible benefits waiting for you at the end of your journey. Let’s connect to discuss everything homeownership has to offer.

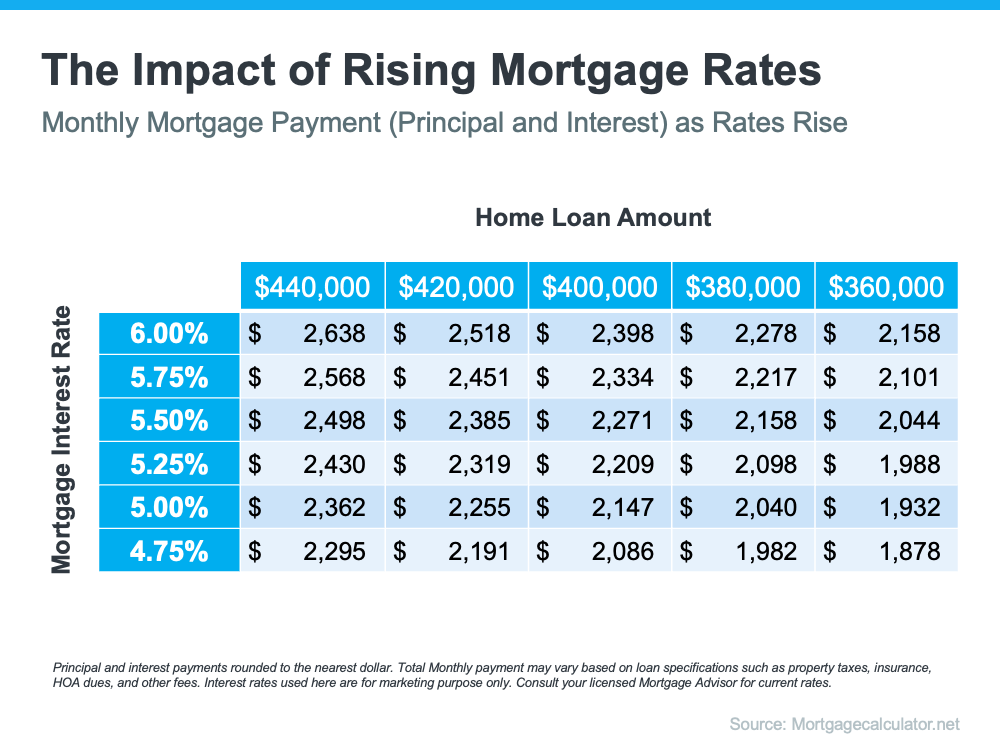

In the last few weeks, the average 30-year fixed mortgage rate from Freddie Mac inched up to 5%. While that news may have you questioning the timing of your home search, the truth is, timing has never been more important. Even though you may be tempted to put your plans on hold in hopes that rates will fall, waiting will only cost you more. Mortgage rates are forecast to continue rising in the year ahead.

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

How Rising Mortgage Rates Impact You

Mortgage rates play a significant role in your home search. As rates go up, they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. Here’s an example of how even a quarter-point increase can have a big impact on your monthly payment (see chart below):

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of delaying your plans, today’s rates should motivate you to purchase now before rates increase more. Use that motivation to energize your search and plan your next steps accordingly.

The best way to prepare is to work with a trusted real estate advisor now. An agent can connect you with a trusted lender, help you adjust your search based on your budget, and make sure you’re ready to act quickly when it’s time to make an offer.

Bottom Line

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Let’s connect today so you can better understand your budget and be prepared to buy your home even before rates climb higher.

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopediaexplains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

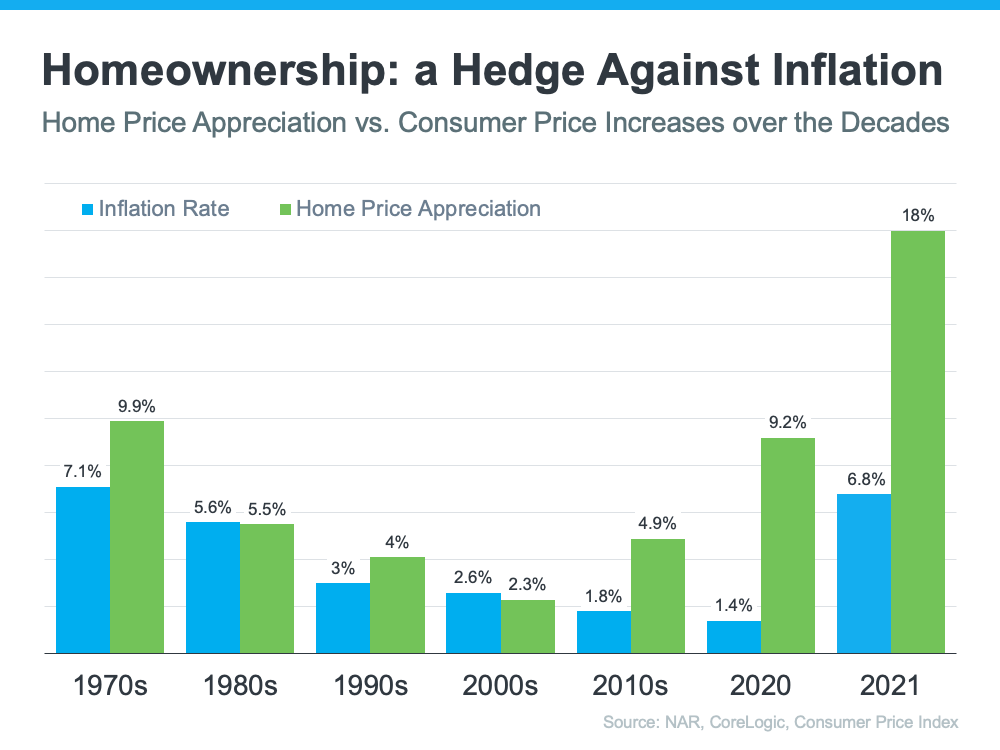

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.